In a world being reshaped by geopolitics, energy intensity, and AI, infrastructure is no longer just a defensive allocation — it is becoming the foundation of the modern economy. Despite its growing strategic importance, we believe listed infrastructure remains undervalued relative to broader equities and consider that this valuation gap presents a compelling opportunity in today’s market.

The state of play

The global investment landscape is navigating a period of profound transition. Investors face an environment defined by heightened geopolitical risks, escalating trade volatility, deep policy uncertainty and substantial technological change. Despite these challenges, global equity indices performed strongly in April and May 2026, rebounding from the sharp sell-off experienced in March to now be back near their highs, mainly supported by resilient earnings and structural growth themes.

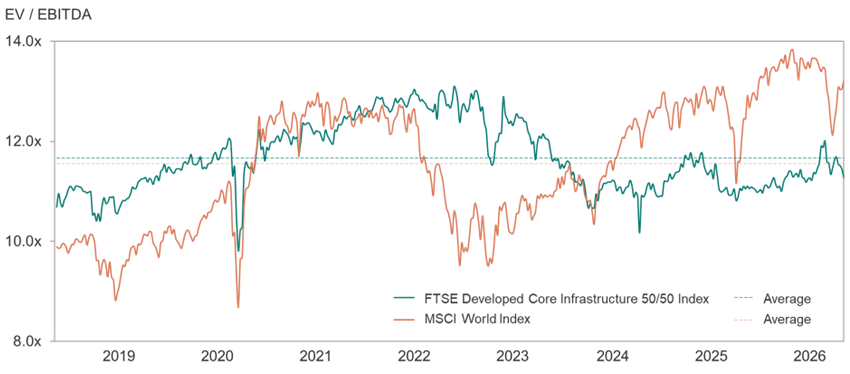

Today, our view is that the valuation gap relative to listed infrastructure remains wide, as highlighted in the chart below. While global equities are trading materially above their long-run valuation range, listed infrastructure remains much closer to its historical norms. For a defensive asset class with growing strategic relevance, that gap is notable. It suggests listed infrastructure has not participated in the same valuation re-rating as broader markets, despite that defensiveness and exposure to many of the same drivers now reshaping the global economy, including rising demand for power, data centre capacity and digital connectivity associated with AI deployment.

Listed infrastructure vs EQUITY VALUATIONS

Source: Bloomberg, 24 May 2026

The infrastructure paradigm redefined

The scale of the infrastructure capital task is substantial. Data from McKinsey indicates that USD 106 trillion in cumulative investment will be required globally through 2040 to meet the demands of global population growth and keep pace with booming technological demand. For investors, this vast capital requirement is an opportunity to access an increasingly wide range of assets that provide the core characteristics of infrastructure.

Geopolitical sovereignty and increasing structural energy intensity are key drivers fundamentally changing the demand for existing and new types of infrastructure. The range of assets that provide infrastructure investment characteristics including inflation protected stable long term cash flows is broadening beyond traditional assets such as roads, airports and utilities to include non-traditional assets that demonstrate key traits: essentiality, resilience, pricing power and long-duration demand. As the economy becomes more digital, electrified, and security-conscious, these characteristics are appearing across non-traditional assets able to respond to the rising demand for the physical systems that support data processing, digital connectivity and reliable power.

Geopolitical fragmentation and national resilience

A growing geopolitical divide worldwide is forcing governments to rethink their reliance on international supply chains and critical services.

This is particularly evident in the realm of digital sovereignty. Data centres have transitioned from basic real estate assets into vital pieces of national infrastructure, drawing intense state scrutiny. Policymakers are increasingly focused on where data is physically stored, who ultimately controls it, and the risk of access being disrupted during geopolitical conflict.

Structural energy intensity

The modern economy is becoming increasingly power-hungry. The rapid expansion of AI, massive data processing centres, and widespread electrification are driving rapidly increasing demand for reliable, always-on energy, and this surge in consumption collides directly with supply constraints. Bringing new power generation and capacity online remains a slow, capital-intensive process, creating a structural imbalance that may favour asset owners.

Energy security has therefore become a matter of state strategy. Governments are now actively aligning policy to support private capital in upgrading generation capacity and grid networks that were not built for today’s demand profile. Commodity market disruption in the Middle East has highlighted the economic cost of dependence on fossil fuels and international supply chains, providing further policy support for energy transition as a pathway to energy security.

It’s worth noting that constraint issues are unlikely to be evenly resolved across regions. Despite policy support, wide regional differences in power costs are set to shift energy-intensive activities to lower-cost regions. This model does however present an opportunity – instead of transporting physical energy, regions with lower-cost power can export digital services such as data processing, cloud capacity or AI workloads, allowing value to flow seamlessly across regions and borders.

Infrastructure: The smarter AI trade

AI is likely to create meaningful disruption across software, services, and other knowledge-based industries. In contrast, physical embedded assets appear materially harder to displace, making listed infrastructure more resilient and in many cases beneficiaries of technological change - something the wider market may not fully reflect.

Additionally, whilst the AI race will inevitably produce clear winners and losers across software and technology, we believe well-placed infrastructure stands to benefit more universally from the same underlying demand. Rather than depending on the ability to pick eventual winners, infrastructure value is captured through ownership of the essential inputs for AI - power, connectivity, and data networks. As a result, selected infrastructure assets which enable this change offer exposure to AI growth largely irrespective of how competitive outcomes evolve at the application layer.

The bottom line

This rare combination of attractive relative valuations, strengthening long-term fundamentals, and defensive characteristics presents a window of opportunity for investors. With government balance sheets heavily stretched by high debt burdens, public funds alone cannot meet the trillions required for this global transition. State reliance on private sector capital has increased materially, securely aligning government policy behind private asset owners.

Listed infrastructure provides a critical anchor of tangible real assets and inflation-protected cash flows and at present, strong visibility over the demand for new and existing assets to support change. Against a backdrop of increasing geopolitical tension and market uncertainty, we believe a combination of defensive characteristics, strengthening fundamentals and attractive relative valuations continue to make a strong case for long-term allocation to listed infrastructure at the entry opportunity offered by current valuations.

To learn more about Morrison Listed Infrastructure visit - Listed infrastructure - Morrison