The widespread adoption of AI applications is increasingly translating into tangible value in early use cases, alongside the initial monetisation of AI platforms. We believe this is sustaining a cyclical uplift across the data centre supply chain and reinforcing a visible multi‑year capital investment cycle, with power and network constraints becoming increasingly binding. The resulting dynamic resembles a reinforcing flywheel, supporting continued investment into defensive infrastructure assets with regulated returns or long‑term, inflation‑linked revenue profiles.

The market focus on AI has already raised awareness of the scale of capital investment required in the infrastructure underpinning compute demand. More recent progress has demonstrated the disruptive capability of more advanced large language models (“LLMs”), the pathway to agentic AI, and drawn a focus on the critical equipment bottlenecks causing a cyclical uplift in the supply chain.

Increased token usage in early adoption is providing greater visibility on the structural challenge of powering AI at scale, as lead times for power generation and network infrastructure struggle to keep pace with the rapid growth in energy demand from both training and inferencing workloads. One emerging response is optimised data centre locations around energy infrastructure, where less latency-sensitive workloads are developed in regions with more readily available and cost-efficient energy, supporting more sustainable scaling of AI infrastructure.

For infrastructure investors, the current acceleration in capital expenditure is likely to extend well beyond the visibility to the end of the decade. Early signs suggest AI adoption is creating a sustained tailwind to infrastructure demand across compute, data and power, reinforcing the opportunity to invest into lower-risk assets with regulated or contracted revenue profiles and embedded inflation protection. Public markets provide a natural access point for to large-scale utility and data centre platforms, while also offering diversification from concentration risk in the AI equity trade.

Demand and Investment Continues to Accelerate

The largest US cloud and AI providers continue to increase their expected capital investment into compute capacity, data centre campuses, networking and power procurement. Market forecasts span a wide range of outcomes but consistently point to investment levels at the limits of physical build capability, placing sustained pressure on supply chains through to 2030. This provides greater investment certainty on acceleration of the capital expenditure cycle with continued demand growth extending the investment cycle beyond the end of the decade. Current market forecasts for 2026 include:

-

Hyperscaler AI capital expenditure of US$670 billion for 20261, with expectations this grows towards US$1.1 trillion in 20272

-

Incremental global IT load demand from data centres rising to 219GW by 2030 (103GW in 2024)3

-

Data centre electricity consumption increasing to 945TWh by 2030 (415TWh in 2024)4

-

Total capital investment in AI infrastructure requirement of US$6.7 trillion by 20305

Early adoption is beginning to support commercial returns

The commercial case for earning a return on capital invested into AI development is beginning to emerge as model capability improves and enterprise adoption moves from experimentation into live workflows. Token utilisation is increasingly rapidly as organisations embed AI into productivity-critical use cases such as software development, customer support, document analysis, financial modelling and workflow automation. The continued development of agentic AI is expected to further amplify this trend, as more AI systems complete multi-step tasks rather than simply respond to discrete prompts. While adoption remains at an early stage, the combination of paid enterprise use, rising query intensity and deeper integration into business processes suggests that demand is increasingly linked to identifiable commercial outcomes rather than speculative experimentation.

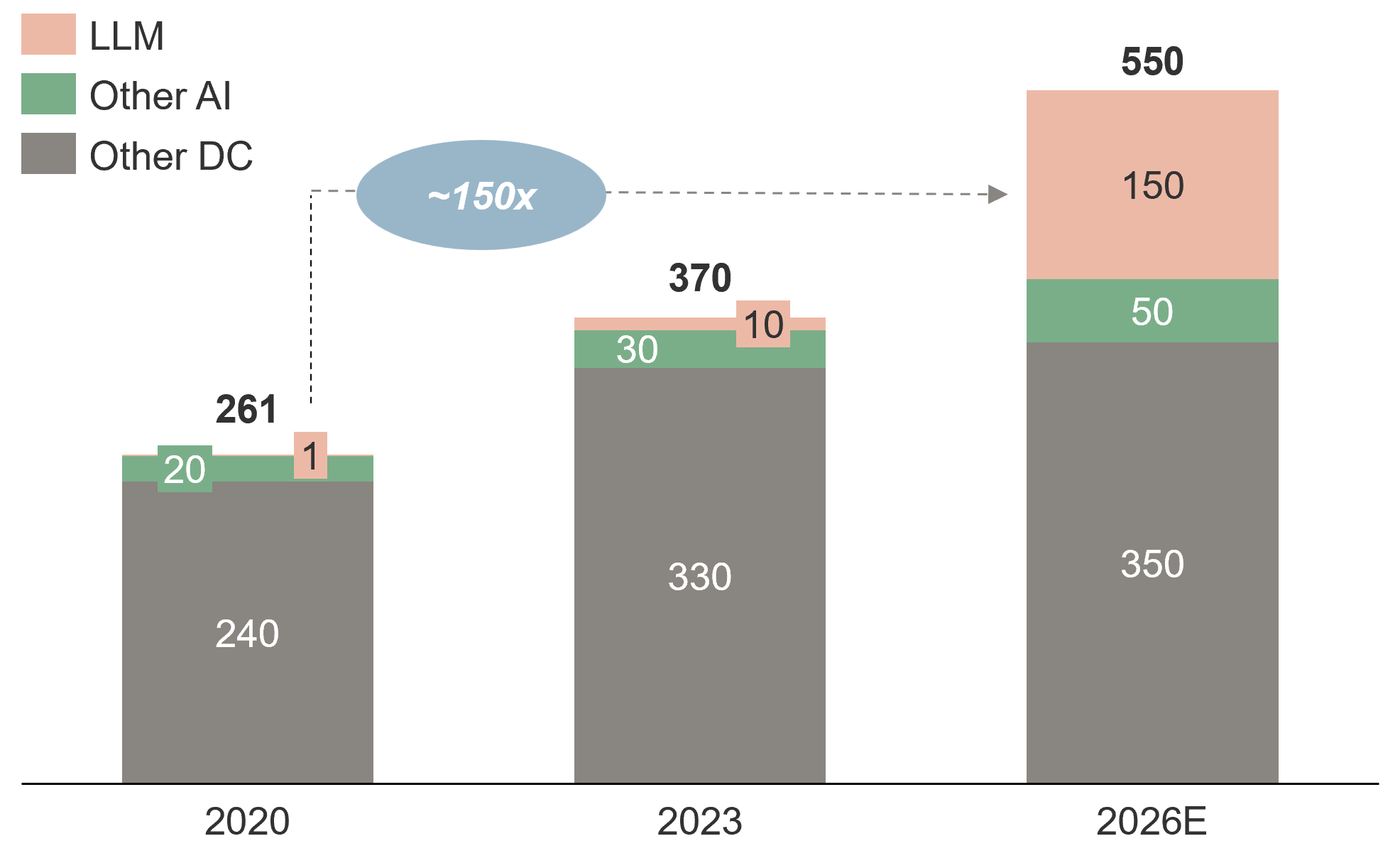

Despite ongoing improvements in compute efficiency, total token demand continues to expand at a faster rate, driving increasing energy requirements. Over the past six years the volume of tokens produced by large language models has been enabled by improvements in compute efficiency of approximately 60 times6, alongside a roughly 150 times increase in energy consumption. Inference now accounts for 60-70%7 of total AI energy consumption and is growing as models scale and adoption deepens.

Data centre (“DC”) energy growth

Increased token usage is driving higher enterprise IT spend. On Uber's Q1 2026 Earnings Call, management confirmed that AI investment had already surpassed its original full-year budget shortly after the first quarter of 2026, describing AI as an accelerator of spending on tools and infrastructure8. Similar patterns are emerging across corporates, with usage controls being introduced to manage costs, but with little change to underlying strategic direction as organisations continue to prioritise AI deployment.

Paid enterprise demand is also beginning to show a credible commercial model where AI is moving beyond experimentation to embedded adoption into core enterprise systems. As use cases broaden and integration deepens, usage is increasingly likely to convert to recurring revenue streams. Microsoft reported rapid growth in Copilot enterprise adoption (>20 million seats at April 20269) and a 20% quarterly increase in queries per user. OpenAI was reported to have reached approximately US$25 billion of annualised revenue by early 2026, while Anthropic was reported to have reached nearly US$19 billion of annualised revenue over a similar period10. Additional disclosure visibility is likely with both companies seeking public listings in 202611 12.

Bottlenecks and Durable Constraints

The pace of AI development is increasingly constrained by the availability of key inputs, including advanced chips, memory and access to baseload power. Supply chain tightness has been most evident in specialised equipment, where shortages have supported margin expansion. While a moat exists for these businesses today, capacity additions are expected to eventually resolve shortfalls in traditionally cyclical industries.

We believe energy, by contrast, is a more enduring bottleneck. The physical lead times required to permit and build generation, transmission and distribution networks mean supply is unlikely to keep pace with the growth in electricity demand driven by AI. Regulatory frameworks, market design and customer affordability considerations further extend the time required to deliver new capacity. As a result, access to reliable power is increasingly a binding constraint on both the pace and location of AI infrastructure development.

Where latency requirements are less critical, AI workloads can be located in regions with more abundant land and energy resources, and more favourable power pricing. These locations must also offer geopolitical stability and trusted operating environments to ensure data security and physical asset protection. We’re observing this dynamic is supporting a degree of regionalisation in data centre development, where the ability to transmit compute output allows power supply to be optimised independently of end-user location.

This trend can be observed emerging across multiple markets. Australia, for example, has seen several large AI data centre project announcements supported by hyperscale commitments13, while China is reported to prepare spending around US$295bn14 over the next five years on a nationwide network of AI data centre hubs. Similar developments are progressing across the UK, Europe, India and other regions, reflecting a broad shift toward geographically diversified infrastructure deployment aligned with energy availability.

Infrastructure investment implications

While the AI thematic presents a broad spectrum of opportunities and risks for all investors, the enduring bottlenecks lie in long duration infrastructure assets which are protected by contracts and regulatory mechanisms supporting approved capex growth and inflation protected cashflows and allowed returns.

Recent developments point to a reinforcing investment dynamic (the AI flywheel), where the continued adoption of AI use cases and ongoing advances in model capability are driving sustained demand for digital and energy infrastructure. The progression toward agentic systems and more complex, compute‑intensive applications further amplifies this trend, extending the visibility and duration of the capital investment cycle across both data and power infrastructure.

Digital infrastructure

We believe large scale contracted data centre portfolios are well positioned to benefit from continued growth in both enterprise colocation demand and AI‑driven compute requirements across training and inference workloads. Asset scarcity will likely lead to upward pricing pressure on contract renewals that is advantageous for existing data centre assets alongside potential improvements in density on existing asset footprints, while regional diversification is providing optionality for a broadening of data centre investment outside the primary US market and is expected to accelerate with an increased focus on data sovereignty and dependence on trusted partners.

A greater focus on underlying infrastructure characteristics will be required to distinguish between business models. Integrated data and power solutions are increasingly attractive where they enable more efficient delivery of large‑scale capacity. In contrast, emerging neo‑cloud models offering GPU‑as‑a‑service are more closely aligned to the lifecycle of hardware and exhibit greater cyclicality than typically associated with infrastructure assets.

Stretched balance sheets are likely to result in recycling of mature data centre asset portfolios, both to listed equity markets and with innovative debt structures. As a result, the pipeline of listed opportunities is expected to expand, providing additional access points for public market investors into the data centre segment.

Powering AI

The near-term commercial advantage has accrued to utilities that are best positioned to respond quickly to emerging power shortfalls, either through advantaged existing assets, supportive regulatory and market structures, or access to the energy resources and equipment required to deliver new capacity. Acceleration of capital expenditure investment is expected to deliver an uplift to earnings growth which is being rewarded by equity markets.

At the same time, we believe the scale and pace of demand growth are reinforcing the need for a broad, technology‑agnostic approach to power supply. Renewable energy remains the lowest‑cost source of incremental generation in many markets, but the magnitude and reliability requirements of AI‑driven load growth will also necessitate additional dispatchable capacity. In the near term, this is likely to be met through gas‑fired generation, while over a longer horizon conventional and emerging forms of nuclear energy are expected to play an increasingly important role in supporting baseload demand.

Connecting large data centre loads and new sources of generation into the transmission network requires new lines and hardening of the existing grid assets. This is creating network congestion and lengthy wait times for new connections in data centre hubs. Behind-the-meter generation may provide shorter term solutions that will ultimately also be optimised by integration to the network for security and redundancy. Transmission system operators and regulators are balancing the demands of generators, utilities and rate paying customers as they update rules and regulations to accommodate large data centre load requirements.

We are observing that dependency on power and the scarcity of compute is causing these large-scale projects to combine as power and data campuses, opening the possibility of selling electrons locally and compute tokens globally. Developing capability in exportable compute will face geopolitical trust issues as AI is more deeply embedded into critical data and systems. The US government shutdown of Anthropic’s Mythos 5 and Fable 5 models this month highlights security and sovereignty issues of international dependence.

Conclusion

We believe AI adoption is providing increased conviction in the sustained infrastructure investment requirement to support additional compute demand. Power is emerging as an enduring constraint likely to present global diversification in both digital and power infrastructure. Tailwinds from AI and digitisation are reinforcing the opportunity for investors to diversify into tangible infrastructure assets with regulated or contracted inflation protected cashflows.

To learn more about Morrison Listed Infrastructure visit - Listed infrastructure - Morrison

1 Source: CDC Investor Day Presentation, May 2026

2 Source: Morgan Stanley Research, May 2026

3 Source: McKinsey & Company, “Scaling bigger, faster, cheaper data centers with smarter designs” April 2025

4 Source: International Energy Agency, “Energy and AI” Report, April 2025

5 Source: McKinsey & Company, “Who’s funding the AI data center boom?” September 2025

6 Source: Morrison estimate,1/W Law Paper Goldman Sachs

7 Source: Manhattan Venture Research - Venture Bytes - October 2025

8 Source: Uber Q1 2026 Earnings Conference Call – May 2026

9 Source: TechCrunch, “Microsoft says it has over 20m paid Copilot users, and they really are using it”, April 2026

10 Source: WinBuzzer, “OpenAI Hits $25b Revenue as Anthropic Closes the Gap”, March 2026

11 Source: Open AI, “Confidential submission of draft S-1 to the SEC”, 8 June 2026

12 Source: Anthropic, “Anthropic confidentially submits draft S-1 to the SEC, 1 June 2026

13 Source: Certified Strategic, “Five themes from a remarkable quarter for Australian data centre and AI infrastructure, 14 May 2026

14 Source: Bloomberg, Charlie Zhu, “China Preps $295 Billion Plan to Fund Nationwide AI Buildout”, June 2026