AI is often discussed as a contest over semiconductors, models and software. Increasingly, however, it is also a contest over power. The compute required to train and run frontier models is driving a surge in data centre demand, and that is turning power infrastructure into a strategic constraint. This matters because although the US still leads in many of the core technologies underpinning AI, that lead will prove difficult to sustain if the physical infrastructure required for deployment cannot keep pace.

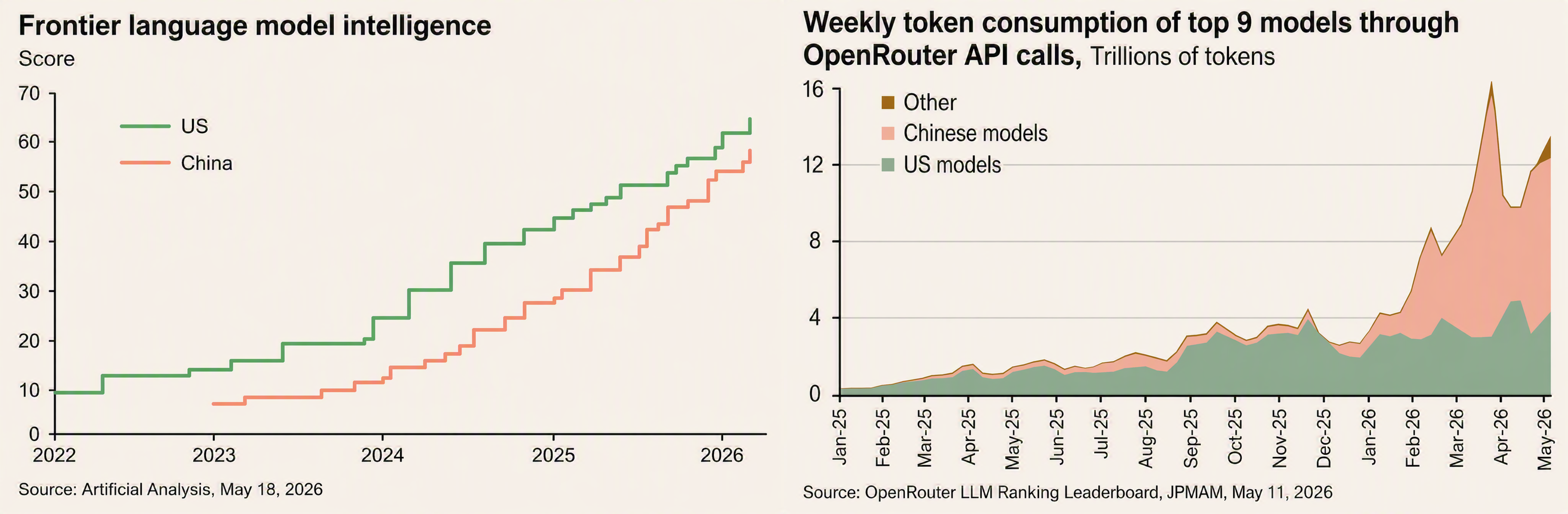

Chinese AI capabilities are not far behind the US, and AI usage is much higher in China

China is using its vast domestic market to scale AI quickly across consumer and enterprise applications, helped by low-cost, open-source models and tightly integrated platforms. At the same time, improving domestic chip capability is helping narrow the compute gap with the West, increasing GPU self-sufficiency and lifting large language model performance. Importantly, competitiveness is increasingly being judged not just by peak chip performance, but by total cost per unit of compute and the ability to deploy at scale. That shift matters because it plays to China’s strengths in low-cost deployment and rapid commercialisation. The sharp rise in token consumption among leading Chinese models in 2026 suggests usage is already scaling quickly, reinforcing the view that China is not just catching up technologically, but also building momentum in real-world adoption.

US VERSUS CHINESE AI CAPABILITIES

Source: J.P. Morgan, Eye on the Market, May 2026

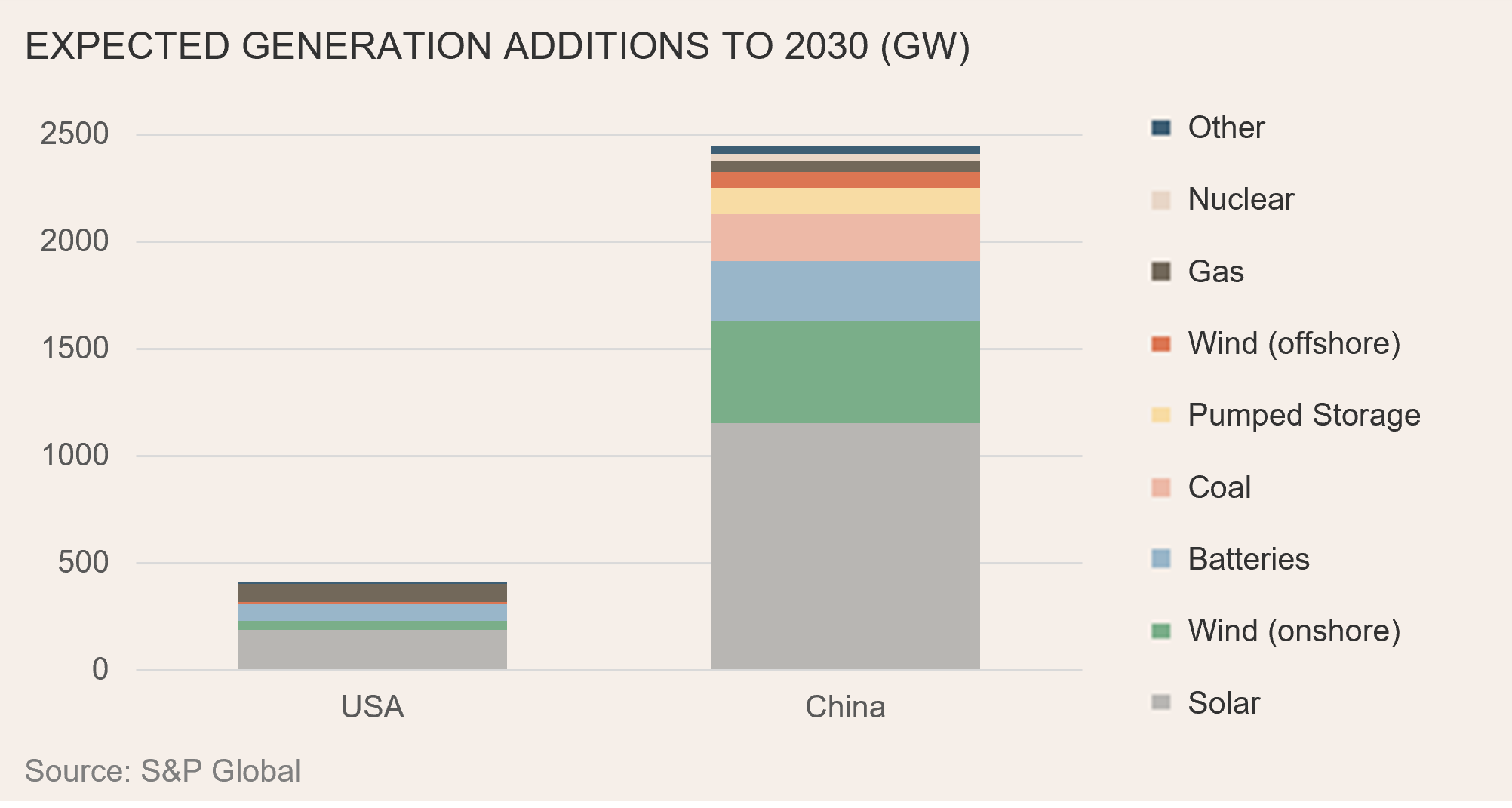

China’s planned generation build-out dwarfs the US

This is where the US-China gap becomes most tangible, given the strategic imperative for each country to develop and control its own AI capabilities. While both countries face rising power needs from AI, China appears structurally less constrained in its ability to supply the required power infrastructure, aided by a more centralised system and a greater willingness to build ahead of demand. In the US, by contrast, growth is often slowed by fragmented regulation, lengthy interconnection queues, transmission bottlenecks and uncertain cost allocation. Indeed by sheer scale, Chinese power generation additions are expected to be 4x that of the US by 2030, with China’s installed generated capacity projected to grow c.60% over the period, vs 25% growth in the US1. If AI is becoming a strategic industry, then resolving roadblocks to power and transmission build-out is no longer just an energy policy issue; it is part of the wider effort to ensure the US remains competitive in the AI race.

Can the US keep up?

This framing of China’s advantage as a more centralised system also explains why in the US vertically integrated utility jurisdictions have been initial winners from the US data centre build out – something we outlined in an earlier article, The Tortoise and the Hare. There we explained that regulated, vertically integrated utilities (the Tortoise) had a practical advantage because they could align generation, transmission and load planning within a single structure, while competitive markets (the Hare) were being held back by interconnection delays, regulatory uncertainty and too many stakeholder interests. In broad terms, that thesis has played out as we anticipated: much of the early market enthusiasm and utility execution has centred on vertically integrated territories that were better positioned to offer clearer timelines and firmer pathways to power.

But the next phase may look different. If the first leg of the AI power story rewarded regulated, vertically integrated utilities, the next leg could create meaningful opportunities for competitive markets as well. For competitive markets, including many of the states in PJM2 (which includes the key data centre state of Virginia) and ERCOT (Texas) the problem has not been the absence of demand (see chart below) or economics; it has been the inability of the market design and regulatory framework to enable the required projects. Data centre demand has exposed those weaknesses sharply, with large load growth pushing up power prices in these markets and in turn politicising and intensifying the debate over how new demand should be connected and who should bear the cost of enabling infrastructure.

![]()

The key difference now is that these obstacles are starting to be addressed. Major player PJM has been moving to reform its interconnection process, improve treatment of large load additions and develop clearer rules for co-located generation and data centre arrangements3. At the same time, local regulators have pushed for greater clarity on how large loads can contract for power without imposing unfair costs on the broader system. Most importantly, PJM is close to finalising rules that would allow direct power contracts between data centre customers and generation developers, paving the way for a potential new wave of announcements regarding capacity additions. Many of these discussions are already well advanced but remain undisclosed, reflecting the political sensitivity around AI and data centre development in several PJM states.

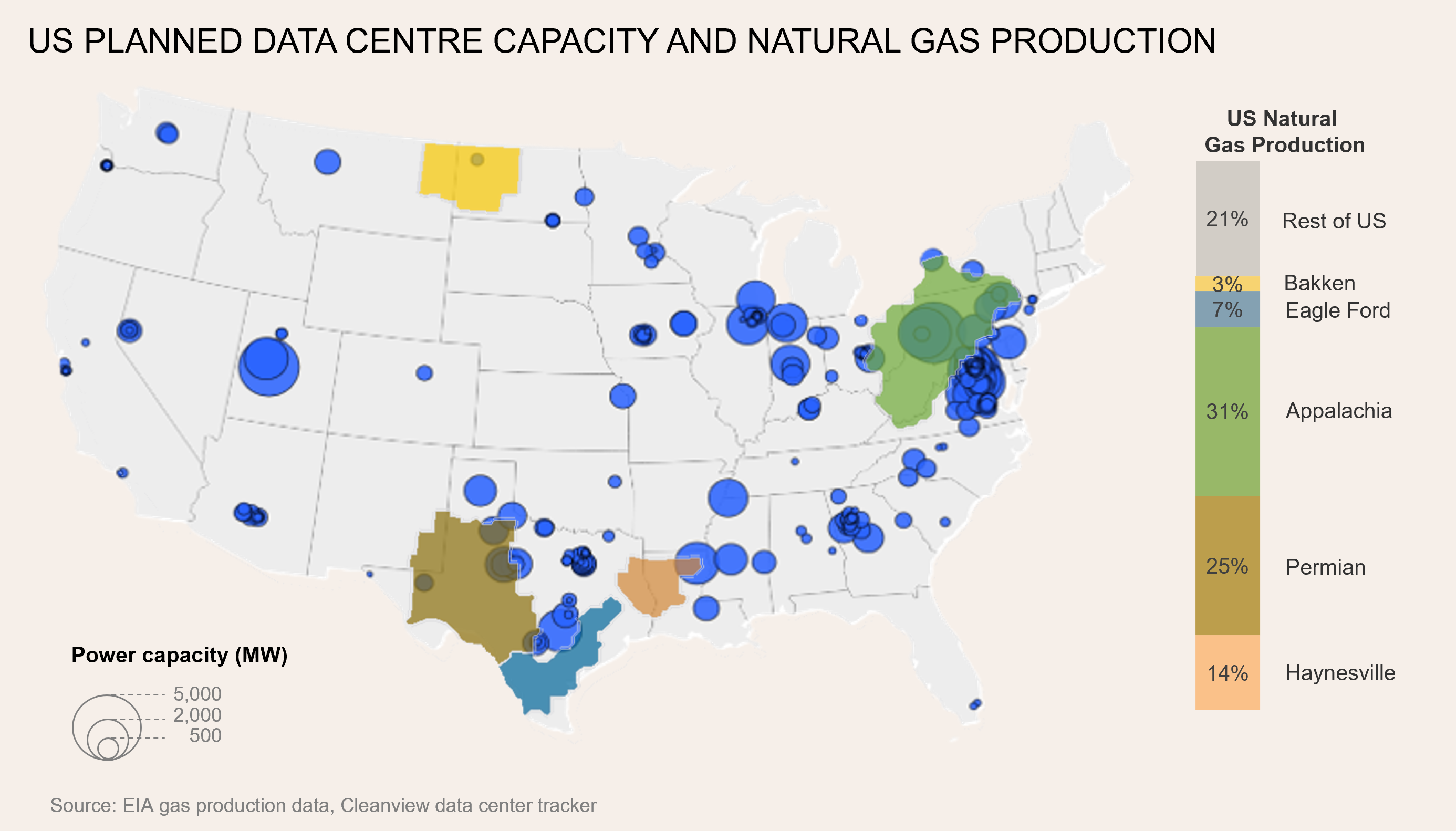

PJM and ERCOT also have important structural advantages over many other jurisdictions because of their proximity to abundant, relatively low-cost natural gas (the Marcellus and Utica basins in PJM and the Permian and Haynesville basins in ERCOT). Combined with existing pipeline infrastructure and land availability, this gives Pennsylvania, Ohio, West Virginia and Texas a natural edge in developing new gas-fired generation to support data centre demand.

Against this backdrop of high data centre demand combined with cheap gas and regulatory unlocking, PJM could become the key region where low-cost Appalachian gas underpins the next phase of AI-related power infrastructure growth. The following chart shows the geographical footprint of data centre demand vs gas supply.

The bottom line

The US does not need a centralised model to unlock the power required to remain competitive in AI, but it does need to remove avoidable frictions that slow investment in generation, transmission and grid access. Addressing these issues in utility markets such as PJM will mark an important step forward, allowing the largest US power market to resume growth and better support the rapid expansion of data centres.

For power and utilities investors, the implication is that the investment opportunity may broaden as the AI power build-out evolves. While vertically integrated utilities were best placed to capture the first wave of data centre load, competitive markets may soon begin to benefit as well. More broadly, infrastructure should benefit regardless of which AI model, application or platform ultimately leads, because while product-side AI may remain volatile, every credible outcome still requires more power. This makes the enabling infrastructure that powers data centres a more durable way to invest in the AI race.

To learn more about Morrison Listed Infrastructure visit - Listed infrastructure - Morrison

[1] PJM, ERCOT, SERC, MISO etc are the electricity system operators in the USA, responsible for electric grid coordination and helping to manage electricity reliability for the states within their service territories

[2] Source: PJM

[3] Source: S&P Global forecasts