Watch Tim Skerman, Head of Listed Assets, explain how we think about the listed infrastructure universe and what sets Morrison’s approach apart.

Christina Eriksson, Executive Director - Listed Infrastructure at Morrison, explores how listed infrastructure provides an evolving universe of opportunities for investors to access essential services, long-duration cash flows, and inflation protection. However, without a universally agreed definition of what qualifies as “infrastructure” in public markets, largely due to the lack of a dedicated Global Industry Classification System for this asset class, it allows managers and indices to define it differently. This means the composition of one infrastructure portfolio can look very different from another, leading to materially different outcomes in returns, volatility, and macro factor sensitivities.

At Morrison we address this challenge by identifying a forward-looking universe of listed infrastructure companies – one that reflects our thematic approach, and commitment to investing wisely in ideas that matter. Here, we share the defining attributes of our universe and explain how it adapts as new infrastructure sectors emerge and societal needs evolve.

We Start with Questions, Not Definitions

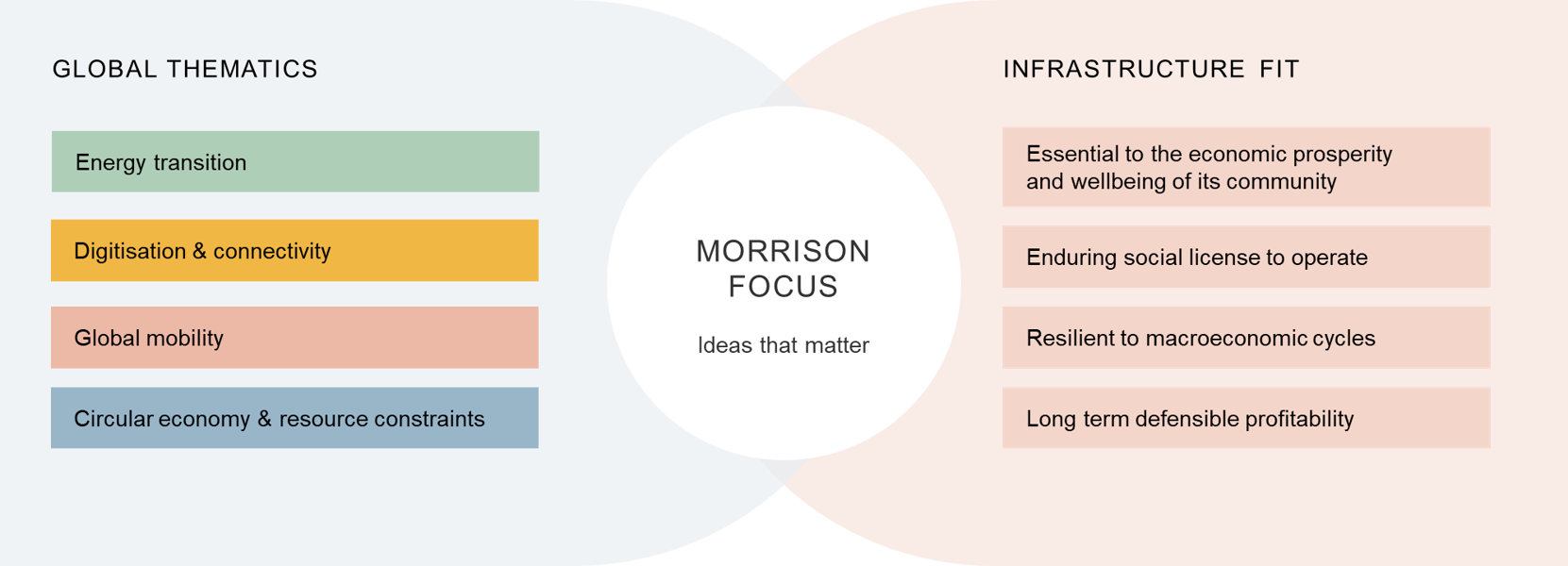

At Morrison, our purpose is to invest wisely in ideas that matter, ideas that address the structural shifts shaping economies and societies over the long term. This philosophy is central to how we define our investable universe. To put that philosophy into practice, we start with curiosity about change. We ask questions like: “How do long-duration forces reshape economies and business models and what does that mean for future infrastructure needs?” This is a fundamentally different starting point which shapes our entire investment process and allows us to invest in assets positioned to benefit from change. These assets share four defining characteristics:

- Essential to economic prosperity and community wellbeing: Infrastructure assets deliver services that are fundamental to the functioning of economies and societies; without an essential role, a business is unlikely to display enduring infrastructure traits.

- Enduring social licence to operate: Long term value creation requires broad based and sustainable community support; assets that cause social harm or lack viability cannot sustain infrastructure-like returns.

- Resilience to macroeconomic cycles: Infrastructure is typically defensible against, though not immune to, macroeconomic cycles, often due to regulated or contracted revenues.

- Long term defensible profitability: Even if not immediately cash-generative, an infrastructure asset needs a clear and credible pathway to sustainable long-term profitability consistent with infrastructure economics.

Our investment universe is positively screened to include companies that meet the above criteria and the requirements of our Responsible Investment Policy. This policy governs what we define as ‘investable’ and helps determine which companies are eligible for inclusion. It sets minimum standards and allows us to focus our research and capital on businesses aligned with long-term value creation and enduring social license.

Our investments in digital infrastructure illustrate Morrison’s curiosity about structural change. We identified digitisation as an enduring thematic by observing long duration shifts in how economies function, with data creation, cloud adoption and connectivity becoming foundational rather than cyclical. We viewed AI not as a separate trend, but as an acceleration of an existing pathway, intensifying demand for data, compute and low latency, and ‘always on’ infrastructure. This thematic lens directed our focus to infrastructure business models at the intersection of data, networks and geography – particularly interconnectivity rich data centres in major metropolitan markets.

Our Universe of Ideas That Matter

Investing wisely in ideas that matter means looking to the structural forces reshaping economies and societies over the long term. There are four enduring global thematics that represent key, long‑term drivers of infrastructure demand in our view:

- Energy Transition & Decarbonisation – covering renewable generation, electricity transmission and distribution, energy storage, and next-generation grid infrastructure

- Digitisation & Connectivity – including fibre networks, data centres, cell towers, and digital infrastructure essential to cloud, enterprise, and AI ecosystems

- Global Mobility – encompassing passenger transit, electric and alternative fuel vehicles, and the infrastructure enabling efficient movement of people and goods

- Circular Economy & Resource Constraints – spanning water treatment, waste management, waste-to-value, and assets addressing resource scarcity

These themes drive how we identify essential infrastructure assets positioned to benefit from long-term demand growth, policy support, and sustained capital investment. Each theme maps naturally to infrastructure business models that deliver critical services and exhibit the durable economic characteristics, for example, tangible assets, high barriers to entry, pricing power, and predictable cash flows.

The outcome is a forward-looking universe of approximately 220 companies that are reviewed quarterly for alignment with our infrastructure definition to ensure the portfolio reflect where the world's infrastructure needs are heading, rather than where they have been. The illustration that follows are the current allocations of that universe.

Universe Allocation by Market Cap

.png)

Source: Morrison. As at 31 March 2026. For illustrative purposes only.

Why Universe Definition Matters

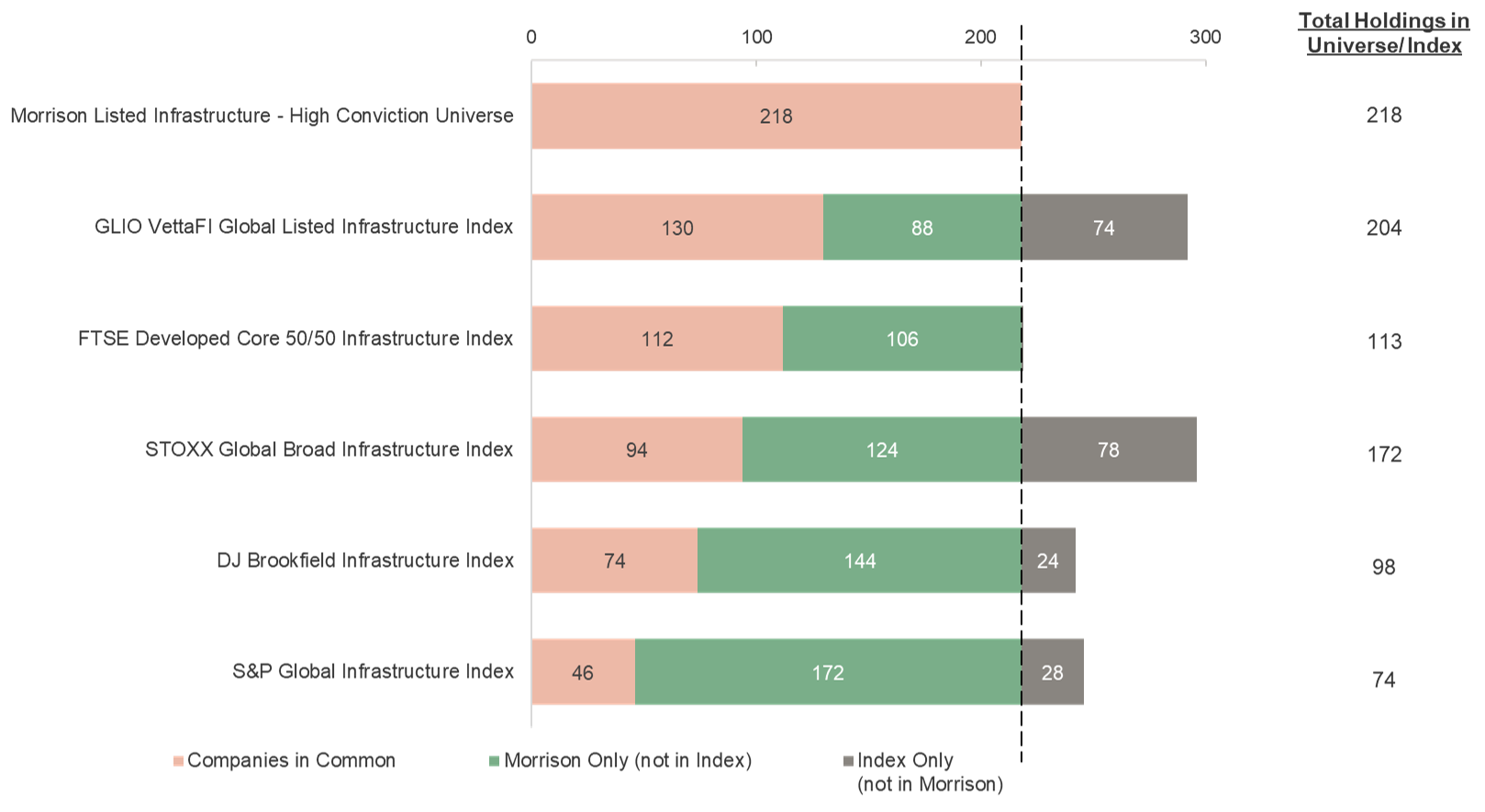

Index construction rules create material investor consequences and as indices take fundamentally different approaches, the resulting sector and sub-sector exposures diverge materially – with implications for return, volatility, and commodity sensitivity.

While infrastructure indices provide a convenient starting point, they often include companies with limited infrastructure characteristics – such as cyclical telecoms or construction firms – whose revenues are volatile, asset bases are intangible, or business models are not aligned with the long-term, defensive profile investors typically seek from infrastructure. One striking example lies in the treatment of renewable energy and clean power: the DJ Brookfield (DJB) Index effectively excludes renewable energy developers (approximately zero allocation), as few companies pass its strict 70% cash-flow-from-infrastructure test.

Our approach results in a universe significantly different from most indices. As illustrated below, we have limited overlap with most infrastructure indices:

DIFFERENCES TO LISTED INFRASTRUCTURE INDICIES

Source: Morrison, Bloomberg as at March 2026

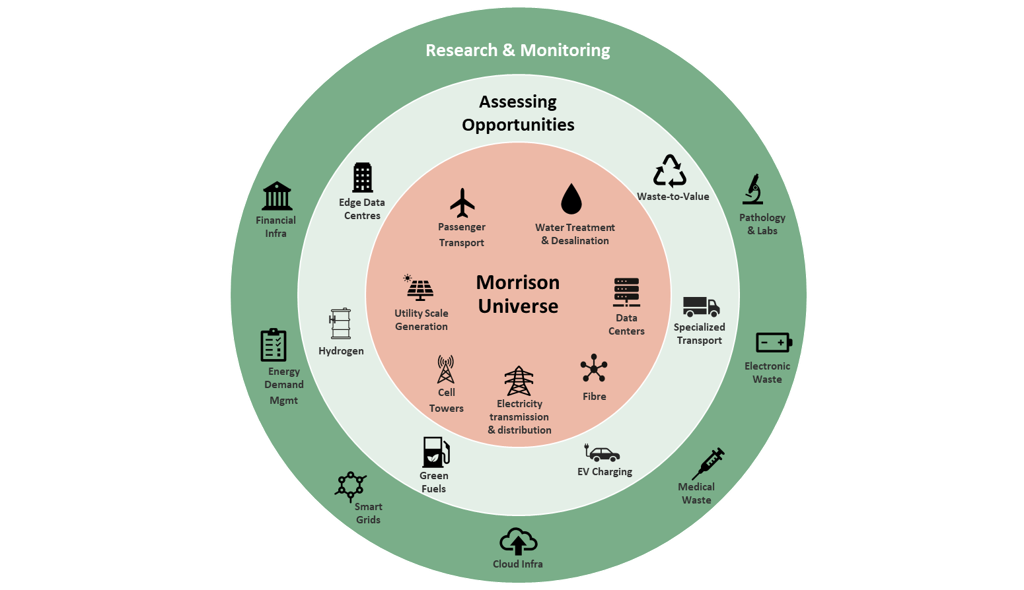

The Opportunity Set: Attributes and Evolution

We maintain an 'emerging pipeline' of sectors and companies under active research – areas where economics, contract structures, or societal roles are evolving in ways that may qualify them for future inclusion as infrastructure. This forward-looking perspective ensures our universe remains dynamic and reflective of infrastructure's changing nature. Examples of subsectors currently under assessment include smart grids, edge data centres, EV charging, electronic waste recycling, hydrogen, and energy demand management, illustrated below.

Source: Morrison. As at 31 March 2026. For illustrative purposes only

As one example, our investment in Equinix exemplifies our ability to identify new emerging sub-sectors early. Equinix provides essential digital infrastructure that enables cloud, enterprise and AI ecosystems to connect and scale, while its control of critical interconnection points creates a defensible advantage that is difficult to replicate. It was Morrison’s experience in managing clients’ direct investment in Canberra Data Centres (‘CDC’, owned by Infratil and other clients since 2016) that has provided the in-depth sector knowledge and capability to build conviction in listed data centre opportunities and supported an investment in Equinix in 2021. To date Equinix has not been included in several widely tracked major infrastructure benchmarks, such as the Dow Jones Brookfield Global Infrastructure Index, the S&P Global Infrastructure Index or the FTSE Developed Core Infrastructure 50/50 Index, demonstrating how our forward‑looking, thematic approach allows us to identify and capture emerging infrastructure opportunities before they are widely recognised. See Appendix I: A Case Study.

In Morrison's view, static, index-based approaches can struggle to capture regional and sub-sector shifts in real time. Indices can be slow to adjust sector weightings or recognise emerging subsectors, often lagging fundamental changes by quarters or years. This creates material risks, such as overexposure to mature or declining sectors, regional concentration, underexposure to emerging infrastructure where structural tailwinds are accelerating, and procyclical concentration as market-cap-weighted indices tilt toward sectors experiencing valuation expansion, regardless of underlying cash-flow quality.

Complementary Universes: Private and Public Infrastructure

At Morrison, we view private and listed infrastructure not as competing options, but as complementary universes within a broader infrastructure opportunity set. Both channels offer access to essential, long-duration assets underpinned by the same core infrastructure economics – tangible asset bases, high barriers to entry, pricing power, and predictable cash flows. However, the way these characteristics are accessed differs across public and private markets.

Privately held infrastructure is shaped by deal flow, bilateral negotiations, and transaction cycles. It can be constrained by deployment pacing, asset availability, and capital lock-up periods. Some opportunities are more aligned to private access, such as early-stage companies or where commercial sensitivities make transparency difficult for markets to assess value.

Listed infrastructure, by contrast, offers continuous access to global markets, enabling investors to dynamically allocate across sectors, geographies, and themes with flexibility and transparency. Some opportunities are more naturally aligned to listed access, such as businesses of large scale and capital intensity. For example, it is very difficult to invest privately in electricity transmission assets that support US power demand growth because of the scale of regulated US utilities.

Our experience managing infrastructure across both universes gives us a unique lens. We apply the same investment philosophy – investing wisely in ideas that matter – regardless of ownership structure. This allows us to assess listed infrastructure assets with the same rigour and discipline we apply to private markets, focusing on the underlying asset quality, regulatory frameworks, and long-term value drivers rather than short-term market sentiment.

Used together, private and listed infrastructure can enhance portfolio diversification, improve implementation flexibility, and broaden exposure to the full spectrum of infrastructure opportunities. A blended allocation allows investors to access sectors and geographies that may be more efficiently reached through one channel than the other, while maintaining a consistent focus on the essential services and structural themes that define the asset class.

Conclusion

How a manager defines the listed infrastructure universe is not a technical detail – it is one of the most consequential strategic decisions in the investment process, which ultimately shapes how portfolios behave across cycles, and whether the allocation delivers the defensive, inflation-linked characteristics that distinguish infrastructure as an asset class.

Benchmark indices, constrained by rules-based methodologies and structural biases, struggle to keep pace with the evolution of infrastructure. Some concentrate excessively in regulated utilities and US equities; others include cyclical businesses with limited infrastructure characteristics; many are structurally slow to recognise emerging subsectors such as digital infrastructure, AI-driven power demand, or next-generation grid assets positioned to benefit from multi-decade structural trends.

Morrison's approach differs fundamentally. By applying a forward-looking lens anchored by enduring thematics, assessed against consistent infrastructure characteristics, and refreshed continuously as subsectors mature – we create an opportunity set that is genuinely diversified, aligned with long-term structural forces, and closely matched to what we believe investors seek when they allocate to listed infrastructure.

In a complex, evolving asset class, the foundation of successful investing lies in identifying and maintaining a dynamic universe. At Morrison, we believe specialist, active management – grounded in deep sector expertise, thematic conviction, and continuous monitoring of the opportunity set – is essential to fully realising the potential of listed infrastructure.

To learn more about Morrison Listed Infrastructure visit - Listed infrastructure - Morrison

Appendix I - A Case Study: How Morrison Identified Digitisation and AI Thematics and Their Connection to Equinix

life across healthcare, commerce, education, finance, and entertainment. The ways in which we create, transmit and consume information are rapidly changing. Morrison has been researching how these developments impact the infrastructure needed to handle the vast amounts of data required to support technological advancement.

Long duration data growth trends, including exponential increases in data generation (growth of ~34% per annum from 2015 to 20201) coupled with dramatically falling computing and storage costs (~45 – 50% reduction in compute costs, and 70 – 85% reduction in storage costs, over the decade to 20192), signalled that demand for data infrastructure would persist and accelerate over decades, not years. Morrison recognised that this wasn't a cyclical technology wave, but a permanent rewiring of economic infrastructure, creating the foundation for the Digitisation & Connectivity thematic.

AI has emerged as an acceleration and deepening of the digitisation thematic, not a standalone trend. Morrison observed that common AI inferencing use cases, such as a Large Language Model (“LLM”) inference request, required approximately 10x the computational power of regular searches3. Future applications (video generation, 3D modelling, design) are expected to drive further explosive growth in demand for computational power. The rise of generative AI, LLMs, and AI-driven applications provided further indications that digital infrastructure needs would intensify, driving the requirement for more capacity, more interconnectivity, and more sophisticated network architectures. This accelerated Morrison's conviction in digitisation as a multi-decade structural theme.

This thematic lens led Morrison to focus on specific infrastructure business models positioned to serve these needs: data centres with interconnectivity platforms, fibre networks enabling data transfer between facilities, wireless towers supporting mobile data consumption, and digital payment infrastructure. When focusing on data centres, Morrison recognised that not all data centre models were equal; interconnectivity-rich, carrier neutral co-location facilities in Tier 1 metro areas would capture disproportionate value when AI inferencing demand accelerated, as enterprises and hyperscalers required low latency, highly connected environments to support hybrid cloud and AI architectures.

We believe that US stock, Equinix, fit the framework precisely: it serves the critical societal need for digital interconnectivity through a business model with infrastructure characteristics (carrier-neutral co-location with ~40% of global hyperscale cloud on-ramp4) and is well positioned to capture long-term value creation from AI inferencing demand. Morrison's investment thesis recognised that Equinix's global leadership in interconnectivity creates a defensible competitive advantage unlikely to be replicated by peers. As AI inferencing architecture mirrors cloud architecture, Equinix's existing ecosystem positions it to benefit from the next wave of digital infrastructure demand without needing to pivot from its core model.

Morrison’s management of CDC, one of Australia’s largest data centre companies, gives the firm deep, first-hand insight into hyperscale and enterprise data centre economics, demand drivers, power and cooling constraints, and customer contracting behaviour. That operational proximity underpins a robust understanding of how AI workloads, cloud adoption, densification, and capital discipline translate into sustainable returns across the data centre value chain. For the listed equities team, this sector level knowledge provides grounding and conviction when underwriting investments in listed data centres such as Equinix: Morrison’s experience with CDC reinforces confidence in the durability of demand, the scarcity value of well located, power secure capacity, and the long-term pricing power of scaled, interconnection rich platforms. The key impact is to reduce information asymmetry and sharpen judgment on where listed market leaders like Equinix are structurally advantaged, supporting a high conviction view on the company’s attractive long-term outlook.

- IDC Global DataSphere & StorageSphere Forecasts; Business Wire summary of IDC data

- Amazon Web Services data from 2019 International Cost Estimating & Analysis Association report “Forecasting Future Amazon Web Services Pricing”

- John Hennessy (Alphabet Chairman), Reuters, February 2023

- Equinix Investor Presentation, Q2 2024