Christina Eriksson, Executive Director - Listed Infrastructure explores the key drivers of listed infrastructure and why we believe it is entering a pivotal moment of opportunity. This article was first published in the Sept/Oct issue of IPE Real Assets.

Listed infrastructure has matured into a recognised core allocation for sophisticated investors. Once considered a niche alternative, it is now often viewed as an integral part of multi-asset portfolios, providing a unique blend of return, stability, and structural growth. Here we highlight why moderating macro pressures and enduring structural growth drivers reinforce the strategic role of the asset class now.

Infrastructure underpins modern life: powering homes and data centres, facilitating the networks that connect businesses and communities, and providing the transport systems that move people and goods. These are essential services, local in delivery, but global in importance, providing stable earnings and resilient cash flows.

At the same time, powerful secular trends are converging. The energy transition, electrification, and digitalisation are reshaping the global economy, driving demand for new generation capacity, upgraded grids, renewable energy, data centres, fibre, and wireless towers. These transformations are capital-intensive, land-constrained, and infrastructure-dependent.

For investors, these characteristics make listed infrastructure both a defensive anchor, offering stability, inflation protection, and lower volatility relative to broader equities, as well as a source of long-term thematic growth aligned with societal priorities. This dual role reflects Morrison’s philosophy of investing in ideas that matter: essential assets that both serve enduring needs and provide sustainable, risk-adjusted returns.

‘Why Now?’: A Convergence of Catalysts

The current environment presents an unusually attractive entry point for long-term investors in listed infrastructure we believe. Two key factors underpin this view:

1. Macro-Inflection Points Provide Valuation Upside

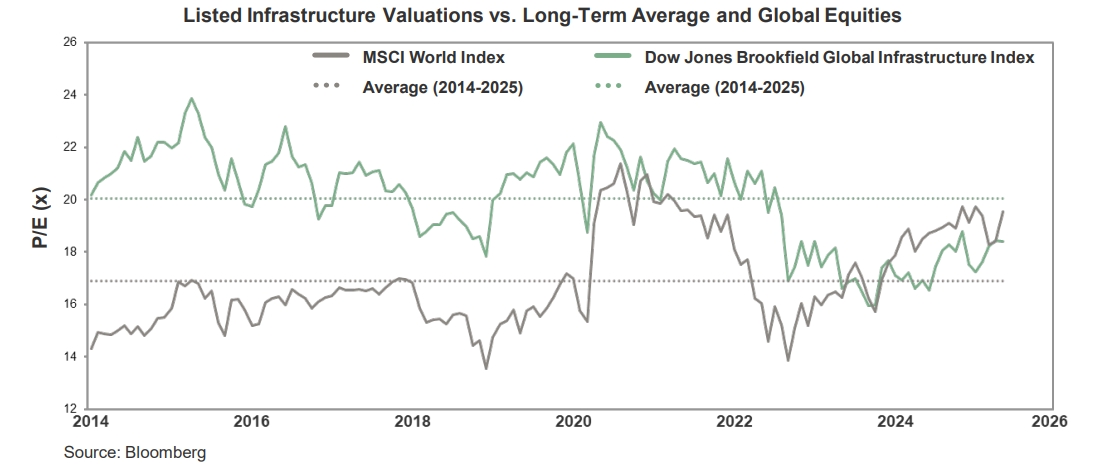

Listed infrastructure valuations are compelling, currently trading at a price-to-earnings multiple of ~18x, below its 10-year average (~20x) and well below the ~23x peak seen over the past five years [1]. Valuations have been constrained by the surge in real interest rates over the past few years, which has moderated in 2024 with European central banks cutting rates over 2024 and expectations that the US Federal Reserve will also cut rates soon as inflation subsides. This is expected to be supportive for the valuation of long-duration assets such as infrastructure.

In contrast, global equity markets have seen meaningful expansion in valuation multiples driven substantially by the growth in a handful of large US technology companies. As of 31 August 2025, the “Magnificent 7” technology companies[2] account for ~34% of the S&P 500 Index and the US represents ~72% of the MSCI World Index, at a time when global equities are touching record highs. The valuation spread between infrastructure and global equities provides investors with an opportunity to diversify into a more defensive asset class backed by tangible real assets with a global footprint. A global perspective is important at a time when geopolitical risk is relatively high, US policy change is leading to uncertainty, and the US dollar is depreciating from the strength seen in recent years.

With earlier macro headwinds fading, investors with a long-term horizon looking to access essential, inflation-linked assets, can now do so at a discount to both history and broader equities.

2. Infrastructure: The Backbone of the Next Decade’s Growth

A set of powerful secular trends are converging, which is expected to reshape economies and capital markets over the coming decades with trillions of dollars of investment required:

Trend 1: Energy Transition & Electrification

The transformation of global energy systems is driving massive capital requirements. Demand for electricity is rising sharply as transport, heating, and industry electrify, and as data centres and digital infrastructure require ever-greater capacity. Meeting this demand will require substantial new generation capacity, grid modernisation, and expanded transmission networks.

For regulated utilities, value creation is not tied to whether they are building solar farms, wind projects, or gas plants. Their regulated frameworks allow them to earn a return on capital deployed into essential assets, whatever the policy mix. Listed utilities and networks are natural beneficiaries of the scale of investment required, independent of carbon and net-zero agendas.

Trend 2: Digital Infrastructure: AI and Data Demand

Artificial intelligence, cloud computing, and demand for data are driving the exponential demand for physical infrastructure assets such as data centres, fibre-optic networks, wireless towers and the power infrastructure to support them all:

- Data centres – Highly power-intensive, land-constrained, and increasingly subject to regulation, data centres are the cornerstone of the AI and cloud ecosystem. Their strategic location near energy and fibre networks makes them difficult to replicate.

- Fibre networks – Serving as the high-capacity, low-latency backbone of the digital economy, fibre provides the essential connectivity for cloud computing, AI applications, and data-intensive services.

- Towers and edge infrastructure – Essential for mobile data, Internet of Things[3] applications, and the emerging augmented and virtual reality ecosystem, towers and edge assets provide the “last mile” of connectivity and low-latency processing capability.

- Power Infrastructure – With massive increases in power demand being forecasted to facilitate data centre growth, there is a huge need for additional investment in power infrastructure. This includes new generation capacity and transmission lines.

Capitalising on the Convergence: Why Listed Infrastructure?

Listed infrastructure is exceptionally well-positioned to capitalise on these trends in the current macro environment. Growth in the asset class can be attributed to the long-term investment case which has been widely published by industry participants and rests on the following core pillars:

1. Attractive net total returns

The stable cashflow profile and secular trends driving demand for infrastructure investment provide an attractive return of both capital and income over a medium-term horizon.

2. Downside protection

Listed infrastructure companies own and operate essential services such as regulated utilities, transport networks, energy pipelines, data infrastructure, whose demand is generally not directly tied to GDP growth. Regulated revenues, long-term contracts, and high barriers to entry help shield performance and stabilise returns during periods of equity market stress.

3. Inflation-protected income

Listed infrastructure is naturally equipped to protect against inflation. Many assets benefit from contractual or regulated pass-through mechanisms – tariffs for utilities, toll roads, and other services are often indexed to CPI, directly preserving real returns. Beyond this, demand for essential services such as energy, transport, and water remains relatively stable even as costs rise, reinforcing revenue resilience. The hard-asset nature of infrastructure, such as pipelines, airports, and grids, provides intrinsic value that can appreciate in real terms during inflationary periods. Finally, the sector’s earnings, often indexed to inflation, create a natural hedge compared with growth-oriented equities.

4. Diversification benefits

Listed infrastructure provides complementary exposure within multi-asset portfolios. While it remains part of the equity universe, its return drivers such as regulated earnings, contracted cash flows and demand for essential services are distinct from those of more cyclical sectors. This differentiation makes listed infrastructure a valuable portfolio component, offering stability and income characteristics that complement traditional equity and fixed income allocations.

5. Liquidity and transparency

Listed infrastructure offers daily liquidity, transparent pricing, and strong governance standards, features valued by clients who require flexibility in their allocations.

Taken together, these attributes explain why listed infrastructure is often regarded as a core allocation in institutional portfolios, rather than solely a short-term opportunity.

Implications for Future Investment Need

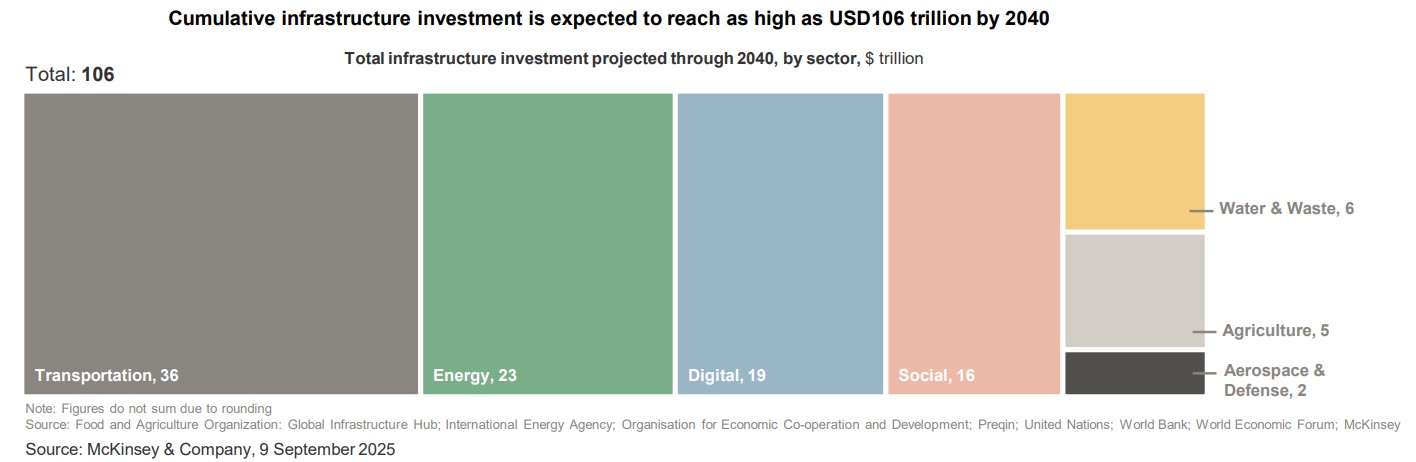

The world is estimated to require USD106 trillion of infrastructure investment by 2040 [4], with energy transition and digital infrastructure accounting for a substantial share. While the investment need is striking in scale, the real question for investors is how this translates into future returns. We believe the answer lies in the mechanics of growth:

- Incumbent Advantage. Existing operators are often structurally advantaged either through scale and network effects or directly as monopolies, such as the electricity transmission and distribution companies which are natural monopolies with exclusive geographic concessions.

- Capital Competition. In regulated sectors, such as utilities, rising competition for capital is pushing up allowed returns as regulators adjust return frameworks to attract global capital. Outside of regulated utilities, companies facing a larger pipeline of projects and opportunities can be more selective and raise hurdle rates.

- Selective Growth. Active managers can identify which projects generate the strongest risk-adjusted returns - an edge in a market where not all USD106 trillion of spend will create shareholder value.

- IPO Activity. Rising infrastructure demand is likely to expand the listed universe as asset owners seek to share the capital burden and return profile with public market investors.

Managing Risks Through Active Investment

2025 has been characterised by global market volatility and geopolitical uncertainty. Morrison’s approach to risk management is embedded in the way we construct portfolios - combining bottom-up company analysis with top-down portfolio positioning to diversify exposures with an aim to capture the highest risk-adjusted returns.

- Bottom-up analysis. Every investment is assessed across multiple dimensions: asset quality, leverage, country risk, FX exposure, and regulatory frameworks. This is supported by the expertise of ~80 professionals, including 35+ sector specialists, and informed by our experience as both listed and private asset owners. Risks are factored directly into our valuation framework, shaping the expected return we require for each company.

- Top-down portfolio construction. We dynamically diversify across sectors and geographies (OECD markets and beyond, subject to UCITS rules), adjusting allocations as risks evolve. This flexibility contrasts with geographically narrow benchmarks or sector-specific funds, allowing us to manage interest-rate, policy, and execution risks more effectively.

- Dynamic positioning. The portfolio leans into secular themes, such as renewables and grids in Europe/UK, digital infrastructure and utilities in North America, while retaining the flexibility to pivot as macro or regulatory conditions shift. This blend of defensive and growth exposures balances risk while aligning with long-term thematic tailwinds.

This integrated process ensures that capital is allocated where we see the greatest excess return potential, a function not only of opportunity but of careful risk pricing and mitigation.

A Rare Opportunity

Listed infrastructure combines essential services, stable cash flows, and inflation protection with attractive long-term returns. With recent underperformance creating a valuation gap just as macro headwinds fade and secular growth accelerates, we believe this is a rare opportunity for long-term investors.

The report can be downloaded as a PDF here.

To learn more about Morrison Listed Infrastructure visit - Listed infrastructure - Morrison