Ben Tedder, Senior Analyst, explores why we expect the "tortoise" of the US regulated electricity sector - the vertically integrated utility – to enable and benefit from the rapid roll-out of data centres across the US.

In the past, vertically integrated electric utilities – a type of utility company that owns assets across the electricity supply chain including generation, transmission, and distribution– have been seen as slow-moving given they operate in monopoly regulated environments that can be resistant to change. In contrast, deregulated electric utilities in competitive markets have been viewed as more adaptable due to less burdensome regulation and the influence of market forces. But a shift is underway.

As data centre power demand skyrockets – driven by cloud computing, artificial intelligence (“AI”) workloads, and digitisation – the ability to deliver large-scale, reliable, and clean(-ish) power quickly becomes a critical differentiator, particularly to the hyperscalers such as Google, Meta, Amazon and Microsoft. Surprisingly, vertically integrated utilities in regulated markets are rising to the challenge faster and more effectively than their counterparts in competitive markets1.

In theory, deregulated electricity markets should be nimble, efficient, and responsive to price signals, thus enabling them to respond effectively to increased electricity demand through new generation (supply). In practice however, competitive markets have faced significant bottlenecks and regulatory challenges to building new generation that is slowing data centre deployment.

THE BACKDROP: DATACENTRE POWER DEMAND SURGE

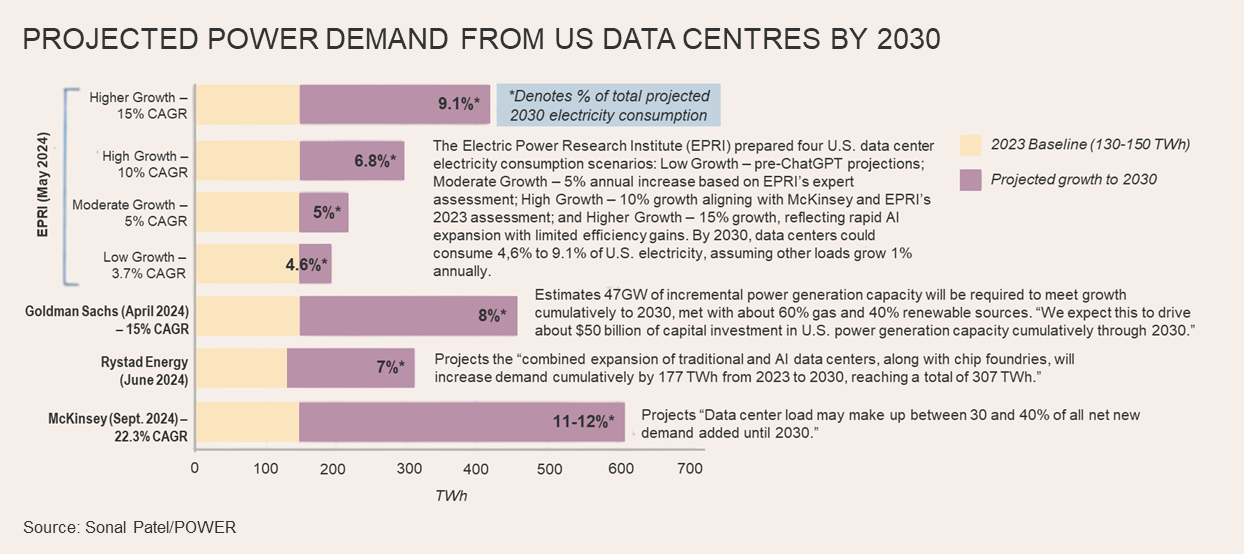

The rise of generative AI, high-performance computing, and exponential growth in cloud services is driving an unprecedented wave of electricity demand. According to industry estimates, US datacentre electricity use could double by 2030, surpassing 400 TWh annually - nearly 10% of total US electricity consumption1 .

Data centre providers and hyperscalers are seeking gigawatts of capacity across multiple US regions. What’s more, they need:

• Speed: Power must be delivered within the next 3-5 years to align with build timelines and AI learning targets of the hyperscalers

• Scale: Individual sites often require hundreds of megawatts (“MW”), if not gigawatts (“GW”), of energy

• Reliability: ’Firm’ (constant) power is required as opposed to the intermittent power delivered by renewables like solar and wind.

• Clean energy pathways: Whilst gas generation is likely to be the only feasible way to deliver firm power in the required timeframe, sustainability commitments demand a contribution from renewable power, particularly on longer-term time horizons (e.g. net zero timeframes)

The surge in demand is therefore not just a matter of increased consumption but also the complexity of power needs. This new power reality exposes friction in how different electricity markets operate - particularly when it comes to project permitting and interconnections, infrastructure build-out, and load planning.

STRUCTURAL BARRIERS IN COMPETITIVE POWER MARKETS

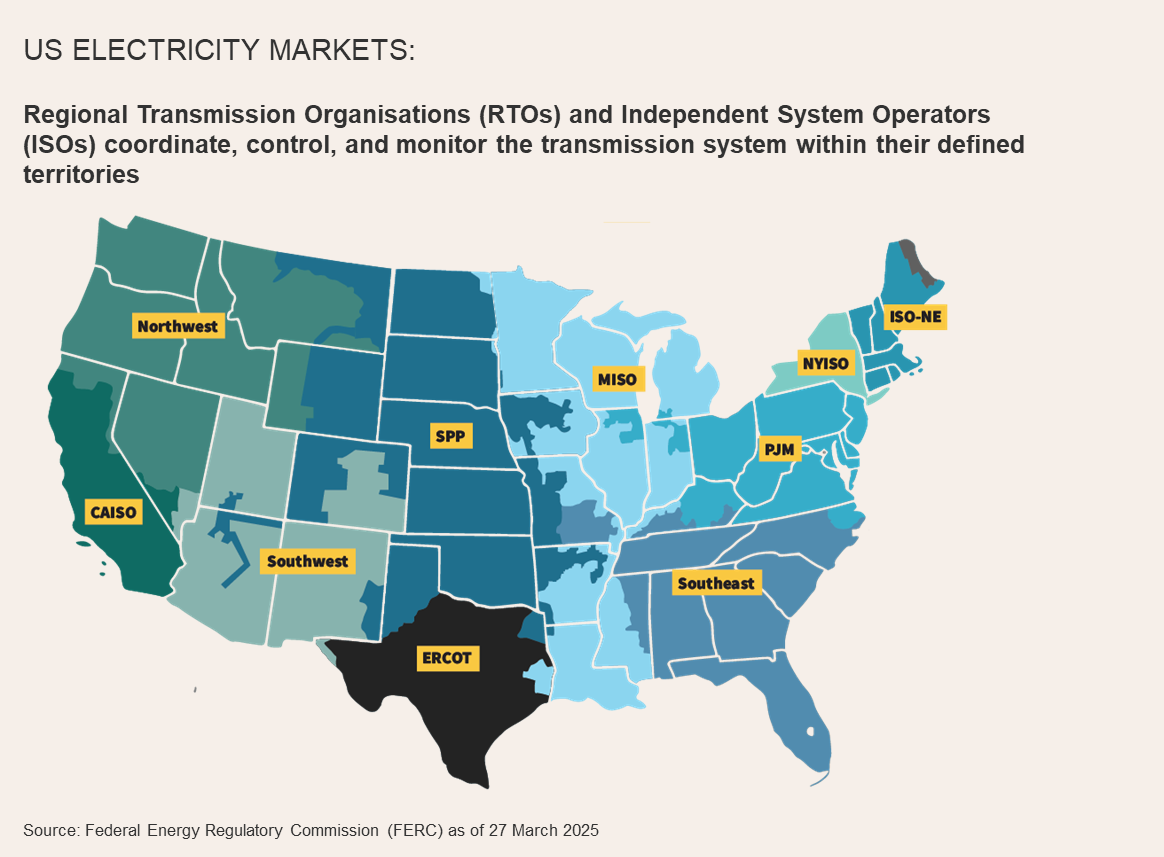

Two major problems in the US electricity market today are interconnection queue delays and transmission congestion. Interconnection refers to the process by which new power generation projects (e.g. wind, solar and gas) and power consumption projects (e.g. data centres) are formally connected to the electric grid, with the start of the process being an application by a developer to enter the interconnection “queue”. This process is inherently complex and time-consuming, requiring coordination between multiple stakeholders including utilities, regulators, local communities and developers. Transmission congestion occurs when the high-voltage lines that transport electricity from where it’s generated to where it’s needed become overloaded or constrained, limiting the flow of power. This occurs when power grids face significant changes in demand (e.g. data centres) and/or supply (e.g. and influx of renewable power) requiring new lines and potentially making previous lines obsolete.

Transmission congestion and interconnection queue delays are impacting the rollout of new power projects in two of the largest US electricity markets, PJM Interconnection and ERCOT (Texas). Studies indicate that projects entering the PJM interconnection queue today have little chance of coming online before 2030, undermining the timelines of power-hungry customers.

In competitive markets, generation, transmission, and distribution are handled by separate entities. In ‘normal’ circumstances where there are no material changes to supply or demand, this can work efficiently where these entities are coordinated to deliver the most efficient power outcomes for the market according to lowest cost principles. However, problems emerge when material demand or supply changes occur and existing processes are not fit for purpose. The bottlenecks in interconnection queues are an example of this and date back years, as renewable energy developers have flooded queues to secure their spots. Moreover, the regulatory landscape in competitive markets can be complex and unpredictable. Changes in market rules, regulatory policies, and tariff structures can create uncertainty and complicate long-term planning for data centre operators. This uncertainty has only been increasing of late, as power markets come under increasing stress and a wide range of stakeholders - including politicians, local communities, developers, and utilities - seek to influence regulatory outcomes to align with their respective interests.

Another aspect of competitive markets is that data centre operators try to minimise their carbon footprint by maximising their utilisation of renewable power, contracting with developers through Power Purchase Agreements (‘PPAs’). However, because the sun doesn’t always shine and the wind doesn’t always blow, renewables can’t provide power all the time. Hence to compensate for this power intermittency, the data centres rely on local utilities to supply the balance, increasing the demand for balancing market services. Together with the lack of visibility around new balancing supply (i.e. gas generation) combined with ongoing uncertainty in market designs (regulatory backdrop), balancing markets are becoming increasingly tight and this is leading to materially higher power costs.

THE UNEXPECTED ADVANTAGE OF VERTICALLY INTEGRATED MARKETS

Vertically integrated utilities operate in regulated environments where power generation, transmission, and distribution are coordinated under a single corporate structure and typically overseen by a single regulator - a model traditionally viewed as centralised, slow-moving, and bureaucratic due to its tight regulatory control. Recently however, this model has revealed unexpected advantages:

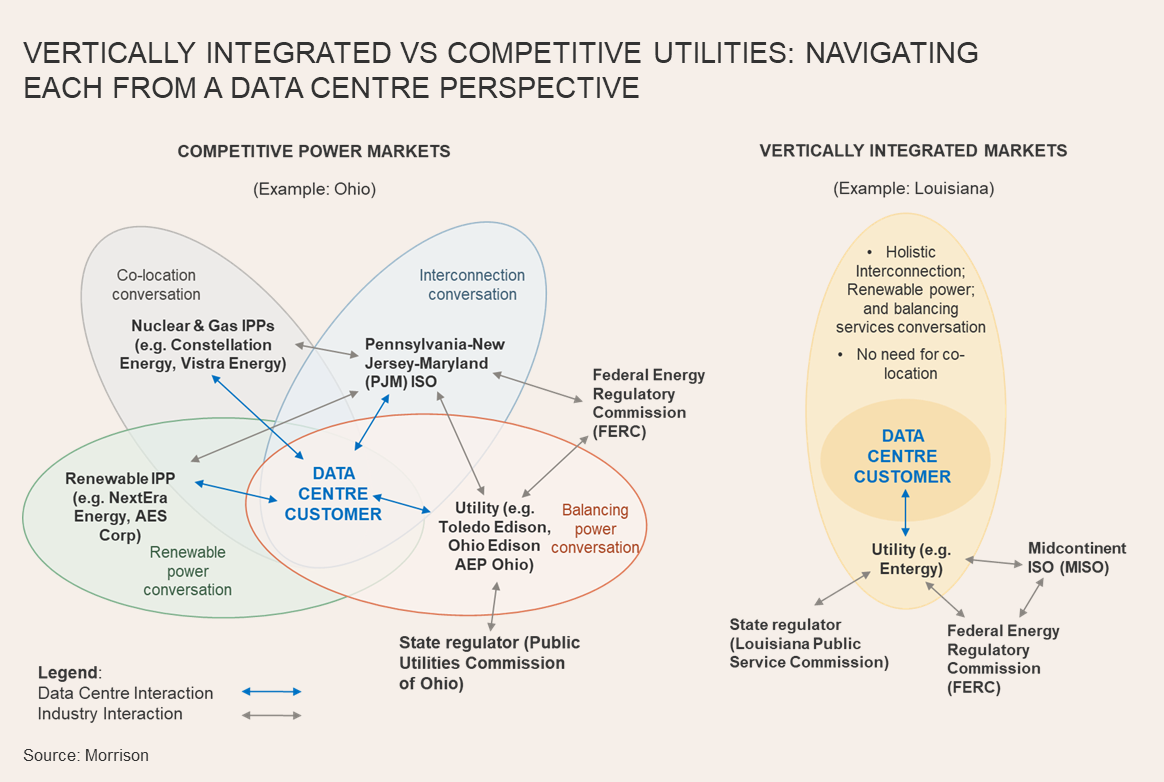

Integrated planning and execution: being able to control all core components of electricity delivery allows for the synchronized development of generation, transmission, and distribution assets, enabling holistic solutions to be developed in a timely and efficient manner. For data centre customers, this control means simplified engagement - instead of navigating multiple processes including interconnection queues, individual PPA negotiations and utility and regulatory processes, they can instead interact with a single entity - the utility. This integrated model also tends to generate data centre customer confidence in both execution timing and cost, given fewer parties are involved and a strong history of successful project execution from such utilities.

Regulatory and policy certainty: in vertically integrated jurisdictions, utilities generally face oversight from a single state-level public utility commission (“PUC”), rather than multiple overlapping regulatory authorities. This relative simplicity also has the potential to allow for tight coordination between utilities, regulators, and political leaders. In several US jurisdictions, state level actors are now unified around a single economic development objective: attracting and enabling high-quality data centre growth. In Georgia, Missouri, and Kansas among others, state policymakers have collaborated with utilities and regulators to pass supportive legislation, streamline permitting, improve regulation and provide tax incentives for large load developments. In supportive jurisdictions, this simplicity fosters a more predictable environment for both the utility and its customers.

Flexible planning: a major misconception about vertically integrated utilities is that they are inflexible due to long, fixed planning cycles. Recent developments in the US demonstrate the opposite: utilities are showing remarkable adaptability in updating their Integrated Resource Plans (“IRPs”) and rate-designs with more frequency. In Georgia, South Carolina and Louisiana utilities such as Duke Energy, Southern Company and Entergy have either updated IRPs mid-cycle to reflect growing data centre demand or stepped out of the IRP process altogether to better find solutions for data centre customers. These and other states are also developing customised electricity rate structures tailored specifically for data centres, aiming to balance the substantial energy demands of these facilities with grid reliability and equitable cost distribution.

The outcome: coordination with Government and Regulators to deliver customised solutions: with these tools in hand, vertically integrated utilities are taking advantage of their centralised structures to co-develop tailored solutions with hyperscaler customers, creating a significant advantage for these utilities over their counterparts in competitive markets.

For example, in 2024, Meta selected Entergy in Louisiana to host a $10 billion data centre project under a fully customised arrangement. Entergy will build over 2GW of gas generation with plans for over 1GW of solar, substation upgrades and a new transmission line, all under a customised 15- year contract with Meta. The amount of investment and value-accretion to Entergy from the deal is significant. To achieve similar outcomes in competitive markets would require aligned coordination across multiple entities, something which is difficult if not impossible to achieve.

THE ROAD AHEAD: REFORM CHALLENGES AND VALUE DIVERGENCE ACROSS MARKET MODELS

Competitive markets will continue to play an important role in data centre development, but significant reforms are necessary to enable the new generation required for an acceleration in data centre demand in their markets. This includes reform of the interconnection process and overall transmission planning. ISOs such as PJM and MISO are already working to overhaul queue management, with new models based on readiness and clustering. Meanwhile the FERC continues to investigate how to encourage proactive, long-range transmission planning.

However, it will take years before these changes bear fruit and the outcome will still likely require alignment across utilities, states, and regional operators.

In the meantime, data centre operators are exploring direct ownership of power assets, utility joint ventures, and co-location / PPA arrangements to circumvent delays in competitive markets. However these solutions, particularly the direct PPA arrangements with nuclear and/or gas generation, do not create new generation capacity and therefore have a limit before local power markets become stressed from undersupply. Therefore, these types of deals are at risk of facing increasing regulatory scrutiny over time until the longer-term problem of new generation capacity is solved in competitive markets.

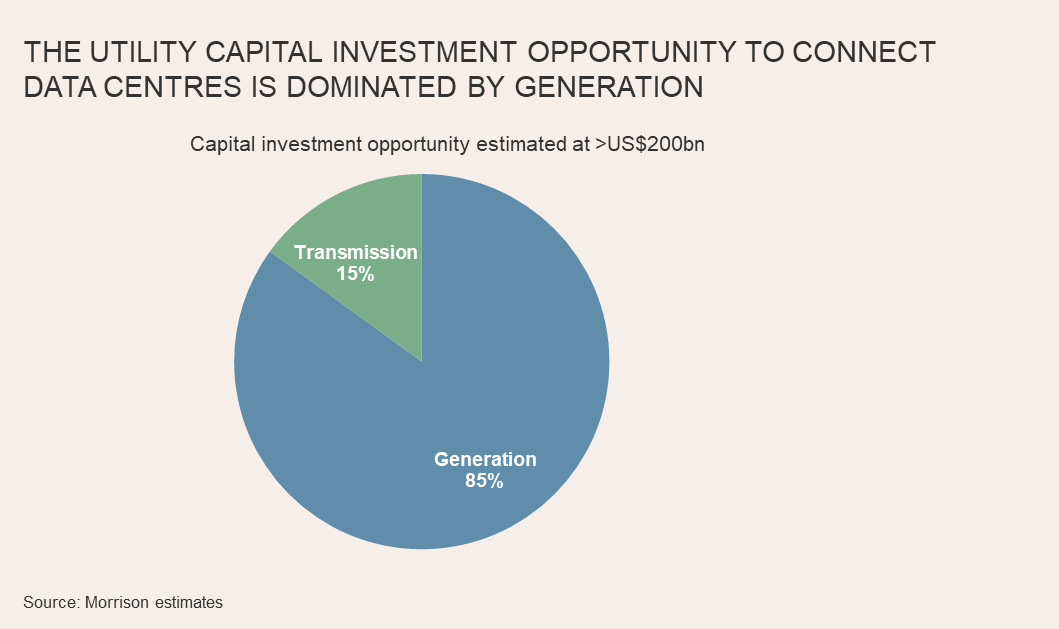

The shareholder value creation opportunity for regulated utilities is far greater in vertically integrated jurisdictions than competitive markets. This is simply because in vertically integrated markets the utilities have a far greater capital investment opportunity, given most of the required investment is in generation assets, unlike utilities in competitive markets that can only invest in transmission and distribution assets. It is no coincidence that in vertically integrated jurisdictions utilities tend to be far more supportive of data centre development. In competitive markets it is the merchant power generators which support data centre development given they are the ones contracting with and benefiting from data centre growth. These generators are higher-risk investments which require a larger return opportunity to compensate for this risk.

CONCLUSION

As digital infrastructure becomes as critical as transportation or water, the energy systems that support it must evolve. While competitive power markets will ultimately evolve to support data centre development, in the near-term their decentralized structure is posing significant challenges when time and coordination are of the essence. Paradoxically, it is the legacy players - vertically integrated utilities - that are proving most capable of meeting the moment and creating shareholder value in the process. With their central control over the required infrastructure, their ability to flex their processes, coordinate across government and regulation all culminating in an ability to provide tailored and timely solutions, they are well-positioned to deliver and benefit from what data centres need most: speed, certainty, and scale.

In the race to power the AI era, the tortoise might just beat the hare.

To learn more about Morrison Listed Infrastructure visit - Listed infrastructure - Morrison