Investment Analyst, Will Parry CFA, explores the key challenges affecting renewable energy valuations, focusing on inflation, interest rates, and declining power prices, and highlights potential investment opportunities in the sector.

It is a widely accepted reality that a huge step up in investment is required to fund the energy transition, with BloombergNEF estimates that US$4.8 trillion is required globally each year to meet net zero. While there is a clear long-term investment requirement and opportunity, the renewable energy sector has faced significant challenges in recent years due to macroeconomic conditions, particularly rising inflation, interest rates, supply chain disruptions, and declining power prices. These factors have exerted downward pressure on valuations of renewable companies in public markets. As interest rates rise, the cost of borrowing also increases, which is particularly challenging for renewable energy projects due to their capital-intensive nature. Public markets have taken the view that future renewable projects in the pipeline of publicly listed companies will either not get developed, or, if they are developed, create little to no value.

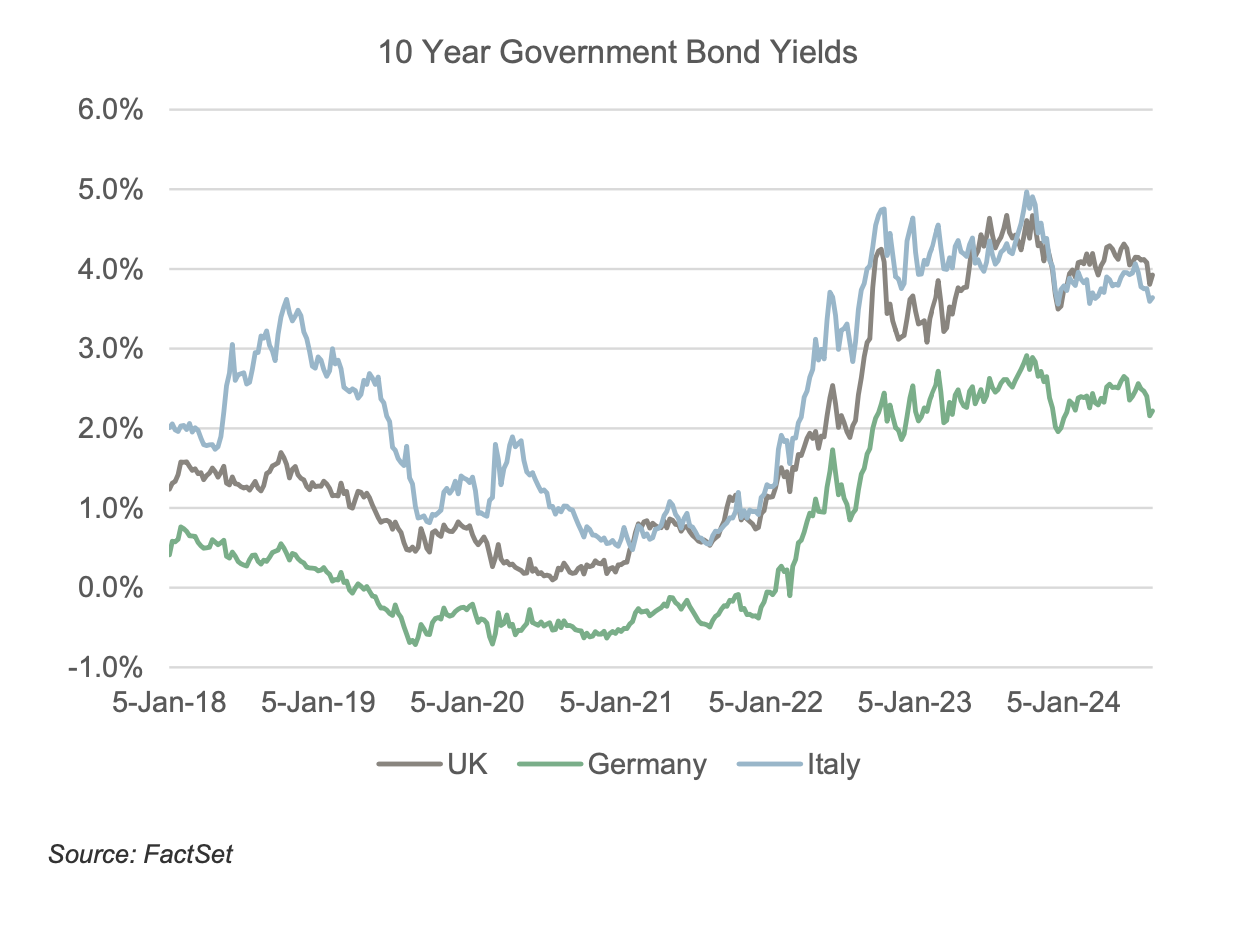

Interest rates have increased, putting upward pressure on the cost of capital of renewable developers

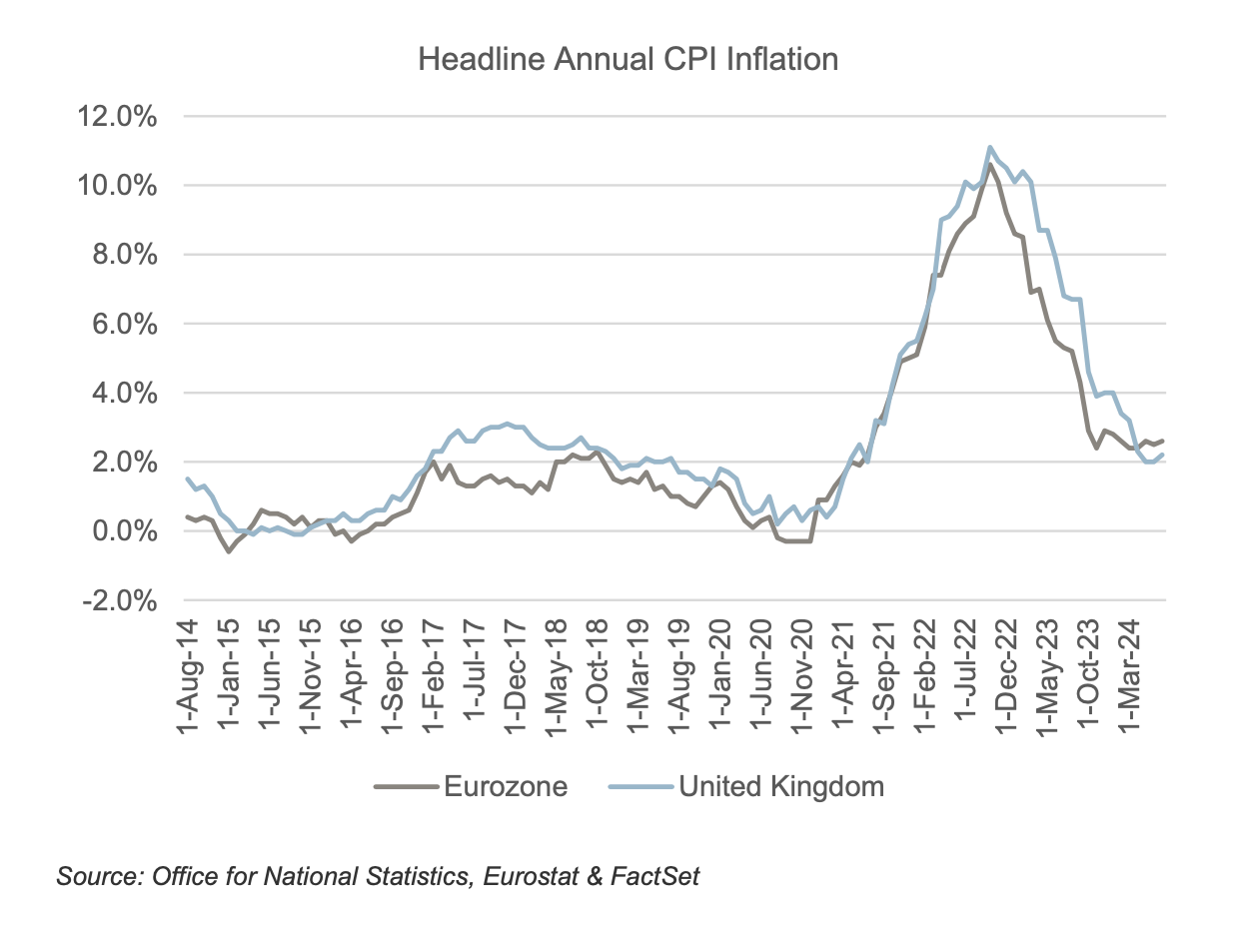

HIGH INFLATION HAS INCREASED PROJECT COSTS

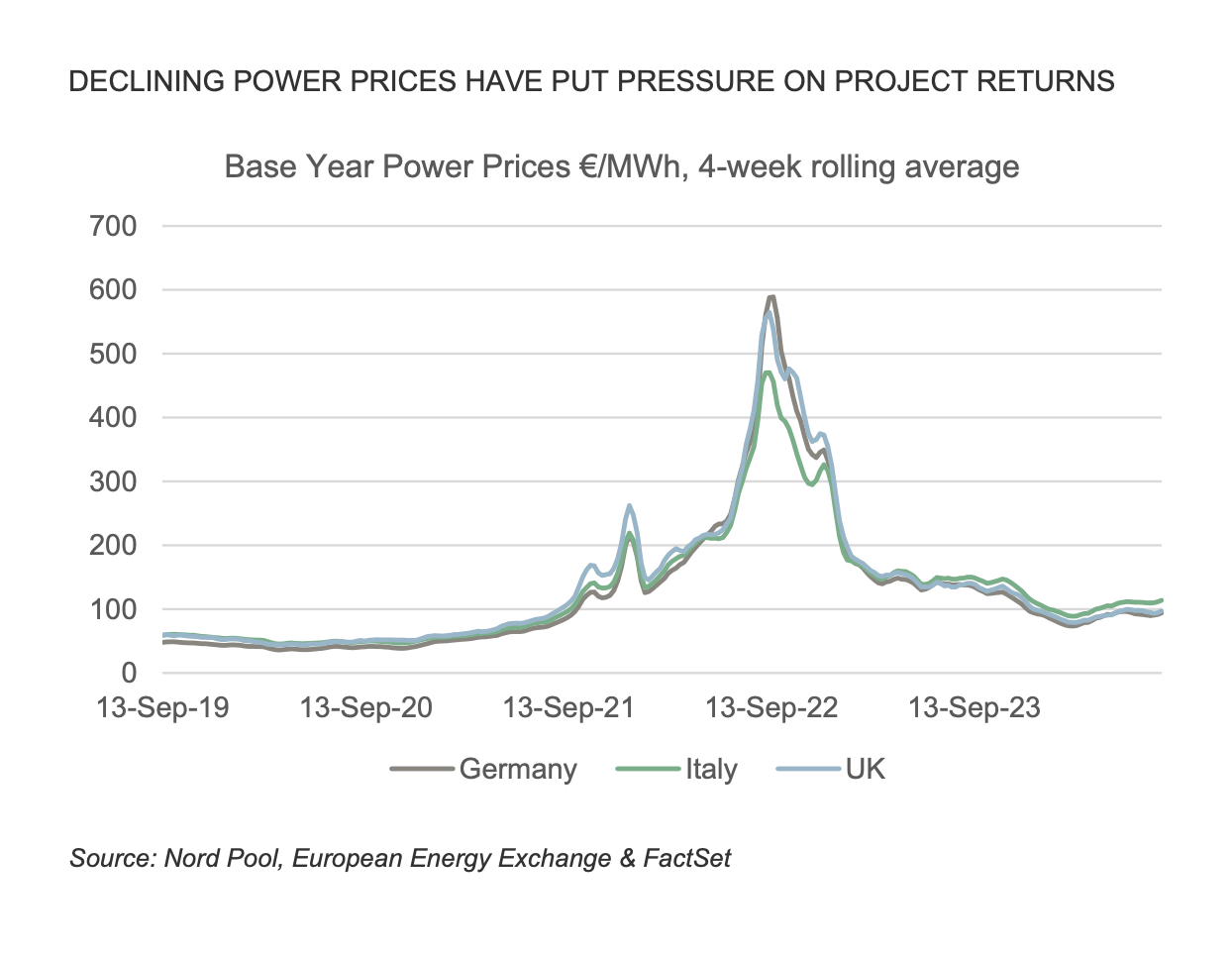

DECLINING POWER PRICES HAVE PUT PRESSURE ON PROJECT RETURNS

Unlike publicly listed renewable companies, private firms often have better access to capital, enabling them to continue project development despite macroeconomic challenges. Private market firms, in particular those with long lock-up periods, can leverage their significant capital reserves and longer investment horizons to weather the aforementioned shorter-term headwinds.

Due to the long-term nature and predictable cash flows of renewable assets, we use internal rate of return (IRR) and net present value (NPV) to assess investments. These approaches capture the full lifecycle of the asset, allowing a more accurate reflection of valuation despite short-term market pressures. As both calculations consider cash flow over the full life of the asset, there is an ability to more accurately capture the valuation impact from temporary headwinds. This valuation approach is consistent with how private markets evaluate opportunities in the sector.

Listed markets, on the other hand, tend to value businesses and renewable assets as a multiple of near-term earnings, cash flow or EBITDA. Given the shorter-term challenges within the renewable sector, we believe that listed markets are overestimating the impact of the current headwinds on the fundamental value of certain businesses. We believe that our approach to valuation over the full life of the renewable asset better reflects the fundamental value.

This different approach to valuation, combined with greater access to capital which enables future development activities, has driven the disparity in valuations between private and public markets. We observe this valuation gap across the sector, even among companies with strong project pipelines and experienced teams.

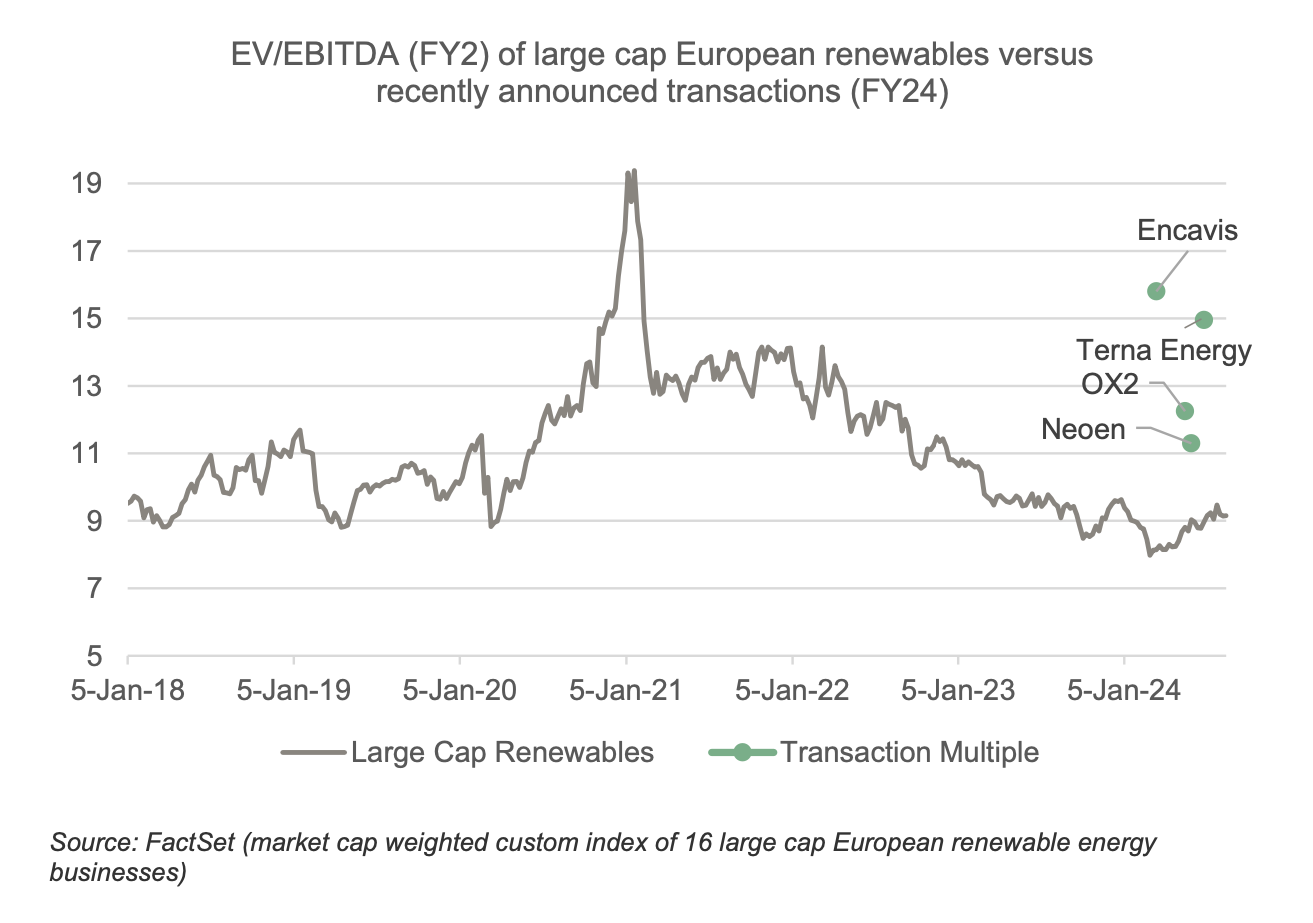

LISTED RENEWABLE ENERGY VALUATIONS WITHIN EUROPE HAVE DECLINED SUBSTANTIALLY IN RECENT YEARS, DRIVING A SPREAD TO PRIVATE MARKET VALUATIONS

This valuation disparity is starting to drive a spate of announcements in the sector. Within Europe, Encavis, Neoen, Terna Energy, OX2, OPD Energy and Greenvolt have attracted interest from private equity players. These moves underscore the confidence that private investors have in the long-term prospects of the renewable energy sector, despite the shorter-term headwinds from inflation and interest rates, power prices and supply chain dislocations.

The premiums associated with these deals so far largely reflects the differences between how public and private markets consider platform value and options for future developments and growth.

The average bid premium in the four largest takeover offers within the European renewable sector so far this year is 28%, versus the 3-month pre-offer price. Given depressed public market valuations, private market funds have been able to invest in listed renewables companies with substantial premiums to pre-announcement share prices, whilst still achieving the 9-11% equity returns hurdle that are typically required by such funds.

PUBLIC-TO-PRIVATE TRANSACTION ANNOUNCEMENTS WITHIN THE LAST 18 MONTHS HAVE BEEN AT A 31% PREMIUM TO UNDISTURBED SHARE PRICES3

![]()

For listed infrastructure investors, this disparity in valuations presents unique opportunities. However, it is important to be selective, as not all renewable energy companies are equally well-positioned. While public market valuations are under pressure, it does not imply that the entire sector is undervalued. It is essential to approach this market with a discerning eye as not all renewable energy companies are created equal. The variability in performance and prospects among public renewables companies requires a selective investment strategy. As sector specialists investing in renewables across both public and private markets since the 90s, we believe we possess the expertise and insights needed to identify opportunities that enables us to capitalize on undervalued assets in the renewable energy space. Morrison is leveraging its expertise to identify undervalued opportunities within the renewable sector, capitalizing on the disparity between public and private market valuations.

[1] Source: https://about.bnef.com/

[2] Includes Neoen, OX2, Encavis and Terna Energy. Volume-weighted average price (VWAP) calculated in the 90 days leading up to the date of each transaction announcement (source: FactSet)

[3] Local currency (€ for OPD Energy, Greenvolt, Encavis, Neoen and Terna Energy, SEK for OX2)

Disclaimer

MARKETING COMMUNICATION

This communication is directed at professional clients.

The statements and opinions expressed in this document and any related discussions (the Document) are based on the information available as at the date of the Document (January 2025) and the information is preliminary in nature only and subject to change, which may be material, at any time without notice. Morrison Private Markets Pty Limited (ABN 71 136 338 906, AFSL No 340502) including its related companies and their respective directors, employees, advisors and shareholders (“Morrison”) reserves the right, but will be under no obligation, to review or amend the Document.

In the UK this Document is issued by Morrison Infrastructure (UK) Limited, Registered in England & Wales under number 11292181. Registered office: CityPoint, 1 Ropemaker St, London EC2Y 9SS. Authorised and regulated by the Financial Conduct Authority.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU). This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The Document and all other information made available to the recipient in connection with it (additional information) do not constitute an offer to invest or the solicitation of an offer to invest or an offer to provide investment management services in any jurisdiction and no such solicitation will be made or offer accepted in the future unless in accordance with appropriate regulatory authorisations in all relevant jurisdictions. The document is not personal financial advice and is not a recommendation by Morrison to make an investment. This Document has been prepared without taking into account the investment objectives, financial situation or particular needs of any particular person or entity. Before making an investment decision, you should consider, with or without the assistance of a financial adviser, whether any investments are appropriate in light of your particular investment needs, objectives and financial circumstances. Nothing contained herein should be construed as legal, business or tax advice and each prospective investor should consult its own advisers as to legal business, financial, tax and related matters concerning the information contained in the Document.

Any person who is in possession of this document is hereby notified that no action has or will be taken that would allow a direct or indirect offering or placement of the units to retail investors in any jurisdiction. No person guarantees the performance of, or rate of return from, products listed in this Document, nor the repayment of capital in relation to an investment in it.

In preparing the Document, Morrison has relied on forecasts and assumptions about future events which, by their nature, are not able to be verified. Inevitably some assumptions may not materialise and unanticipated events and circumstances are likely to occur. Therefore, actual results in the future will vary from the forecasts which Morrison has relied for the purposes of the Document. These variations may be material. Past performance is not a guide to future performance

References to specific company stocks should not be construed as recommendations or investment advice. The statements and opinions are subject to change at any time, based on market and other conditions. Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions. Investing involves risk including the risk of loss of principal.

In addition, the Document contains information sourced from third parties which has not been independently verified. Morrison will not be liable to any recipient for errors or omissions from the Document, whether arising out of negligence or otherwise.