Tim Skerman, Head of Listed Markets, explores listed infrastructure opportunities linked to artificial intelligence in this article first published in the Nordic Fund Selection Journal.

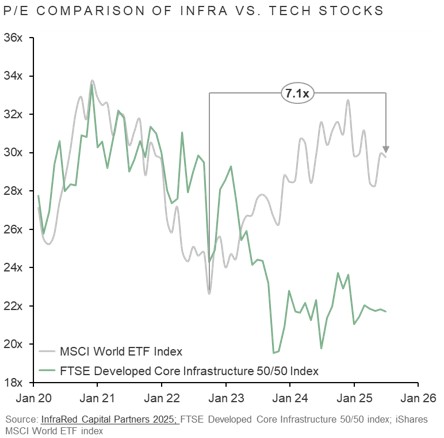

Equity markets are again pushing all-time highs this quarter, fuelled by the continued growth in large cap US technology stocks engaged in the development of artificial intelligence. These stocks have also become a high proportion of the S&P 500 Index and contributed to the increasingly high concentration of US listed stocks represented in global equity indices. It is natural in this environment of elevated tech valuations and concentrated exposure for investors to ask about the potential for infrastructure to provide diversification and downside protection to portfolios.

The listed infrastructure asset class is known for its stable, inflation linked cash flows backed by real assets that deliver essential services such as transport networks and utilities. Investors in the space typically seek its liquidity, defensive characteristics and portfolio diversification, with a return profile from a mix of capital gains and income.

Long term secular trends are instrumental in shaping our current needs for infrastructure and the demand for new infrastructure to support the prosperous and sustainable communities of the future. The technological advance in computing technology enabling the development of artificial intelligence is progressing at a faster pace than the physical capacity to construct the data centre, power supply and fibre network infrastructure required to house the flow of high-power processing chips from Nvidia and others.

At Morrison we believe investing in the infrastructure enabling AI is an ‘idea that matters’ and are seeking to participate in public markets where we see an excess return over risk on our investments. AI related infrastructure investment was the primary driver (92%) of US GDP growth in the first half of 2025 while still only representing 4% of total GDP (Source: fortune.com, Nick Lichtenburg, 7 October 2025). Price to earnings multiple valuations of global equities have expanded in recent years as the AI trade has gained traction, yet global infrastructure equities remain at attractive valuation levels. This article explores the defensive characteristics of US data centre and electrical infrastructure companies, highlighting some of the factors that provide protection to fundamental asset value and their role as resilient assets in diversified portfolios.

Strong Demand Creates a Defensive Moat for Critical Infrastructure

Over the course of 2025, the expected capital spend by large technology firms on the development of AI has accelerated and is now estimated to have grown to $364bn per annum (Source: Yahoo!Finance, Laura Bratton, 2 August 2025). Further, McKinsey expects that data centres equipped to handle AI processing loads to require $5.2 trillion in capital investment globally by 2030 (Source: McKinsey Quarterly, 28 April 2025), and we expect a substantial portion of that will be focused on the US market based on the current level of activity. The surge in demand for data centres and power infrastructure far exceeds the pace at which physical infrastructure can be constructed, particularly power assets which are experiencing multi-year queues for power generation turbines and grid connections. Existing data centre capacity and the value of firm power generation assets or contracts are experiencing strong upward pricing pressure and growing margins because of these constraints.

This market dynamic has created a defensive moat around critical infrastructure assets required to house and operate AI compute. In the case of data centres specifically, the moat is underpinned by high barriers to entry, particularly the capital intensity, long lead times for key equipment and the highly complex designs required to meet the requirements of hyperscale customers, as well as regulatory and zoning complexities. Strategic access to power and fibre connectivity in key regions like Northern Virginia and Dallas further limits new competition. Tenants tend to be highly sticky in the current supply shortage, alongside pre-existing factors including the high switching costs of migrating infrastructure. New data centre designs to accommodate scalable cooling systems and other AI optimisation add a further layer of defence as the technology evolves to higher power densities. The scale and interconnection of leading operators’ data ecosystems create additional network effects for connectivity. With vacancy rates at very low levels and most new capacity pre-leased, supply constraints are expected to persist, protecting the value of data centre assets with access to firm power contracts while demand continues to substantially exceed supply.

Contracted Capacity

Contract structures also provide protection for cashflows on long duration assets. Data centres have a range of contract durations, from short term for higher priced enterprise colocation customers through to as long as 15 years for larger capacity hyperscale contracts. We estimate the average contract duration to be approximately 3-5 years, while noting that many of these contracts will likely be renewed at the prevailing market price due to the costly and time-consuming process of migrating workloads. Tenants will often sign leases that include renewal options, with pre-leasing contracts for new capacity currently being signed as far out as 2028/29. Independent Power Producers (IPP) including renewable energy developers have seen Power Purchase Agreements signed with longer durations (15-25 years) and the clearing price for available capacity has been increasing in markets where capacity is auctioned. Increasingly, intermittent power is being sold alongside battery energy storage system contracts to provide the firm capacity needed to match a data centre customer load profile.

Regulated Capital

In many US states, utilities that provide power generation and/or electricity transmission network infrastructure are regulated monopolies that must secure regulatory approval for capex required to support the development of power infrastructure aimed at meeting new sources of demand or changes in load requirements. Regulators assess the submissions for approval and inclusion of additional capital investment into the asset base on which the utility is allowed to earn a regulated return from customer bills. The increase in demand for power assets has driven an acceleration in utility capital investment underpinned by the stability and risk protection of regulated cash flows.

Capital Structure

Public companies typically have a more conservative capital structure with lower levels of debt than private companies, ensuring an appropriate credit rating that maintains the company’s access to an efficient cost of corporate debt issuance. This approach provides a lower overall level of risk but at a higher cost of capital. As well as working with industry participants, large technology companies are also actively investing in their own data centre and power infrastructure (largely behind-the-meter generation) as ‘time to power’ is critical for progressing the speed of artificial intelligence capability and ensuring high value hardware such as semiconductors are not idle. While this is investment is critical early in development, we do expect public markets to play a larger role in ownership as these assets mature, and strategic control becomes less critical to large technology companies.

Active Investment Positioning

Our High Conviction Infrastructure Strategy is actively invested into data centre providers globally with a skew to dominant activity in the US market. At the end of 3Q25 our allocation to data centre companies represented 12% of the strategy. We also held 21% in US utilities with a preference for vertically integrated utilities we believe will capture the best risk adjusted returns from the growth in US power demand. We consider these allocations to be well protected from potential inflationary pressures of US imposed tariffs, potential beneficiaries of a declining rate environment and of lower political risk given the current administration’s engagement with the sector as a national priority. The strategy seeks to optimise total returns over a medium to long term horizon and is aligned with secular trends driving the demand for infrastructure including digitalisation, decarbonisation, mobility and others.

This article can be downloaded as a PDF here.

To learn more about Morrison Listed Infrastructure visit - Listed infrastructure - Morrison