Investment analyst, Will Harris CFA, explores the global investment landscape of 2025 – which is poised to be both dynamic and complex, a reflection of the rapid shifts in technology, politics, and sustainability that continue to shape our world

- The Republican party’s sweep of US elections in 2024 has powerful and unpredictable implications. It is likely to drive strong near-term growth in the US, while also spurring inflation

- Artificial Intelligence (AI) will remain a dominant theme in 2025 as AI applications begin to permeate businesses and households

- The energy transition will become more regionalised. Attractive investment opportunities for long-term capital are likely

Reflections on 2024

2024 was marked by sustained global economic growth, significant political developments, ongoing technological advancements and strong equity market performance.

Economically, significant progress was made to tame generationally high inflation in many developed markets, though the final stages of this effort remain elusive. In politics, the most consequential event of 2024 was Donald Trump’s election victory and the Republican Party’s sweep of Congress. Technologically, AI continued to evolve with more advanced software and hardware coming to market.

Equity markets generated strong returns, with a total return for the S&P500 of 25% (reaching all-time highs), while other major gauges including the key European index (the STOXX600) and the MSCI World Index also reached peak levels. The impressive performance of the S&P500 was marked by narrow breadth, with most gains concentrated among a small group of technology-driven stocks. Communication Services (+40%) and Information Technology (+36%) were standout sectors, buoyed by a number of factors including surging interest in AI.

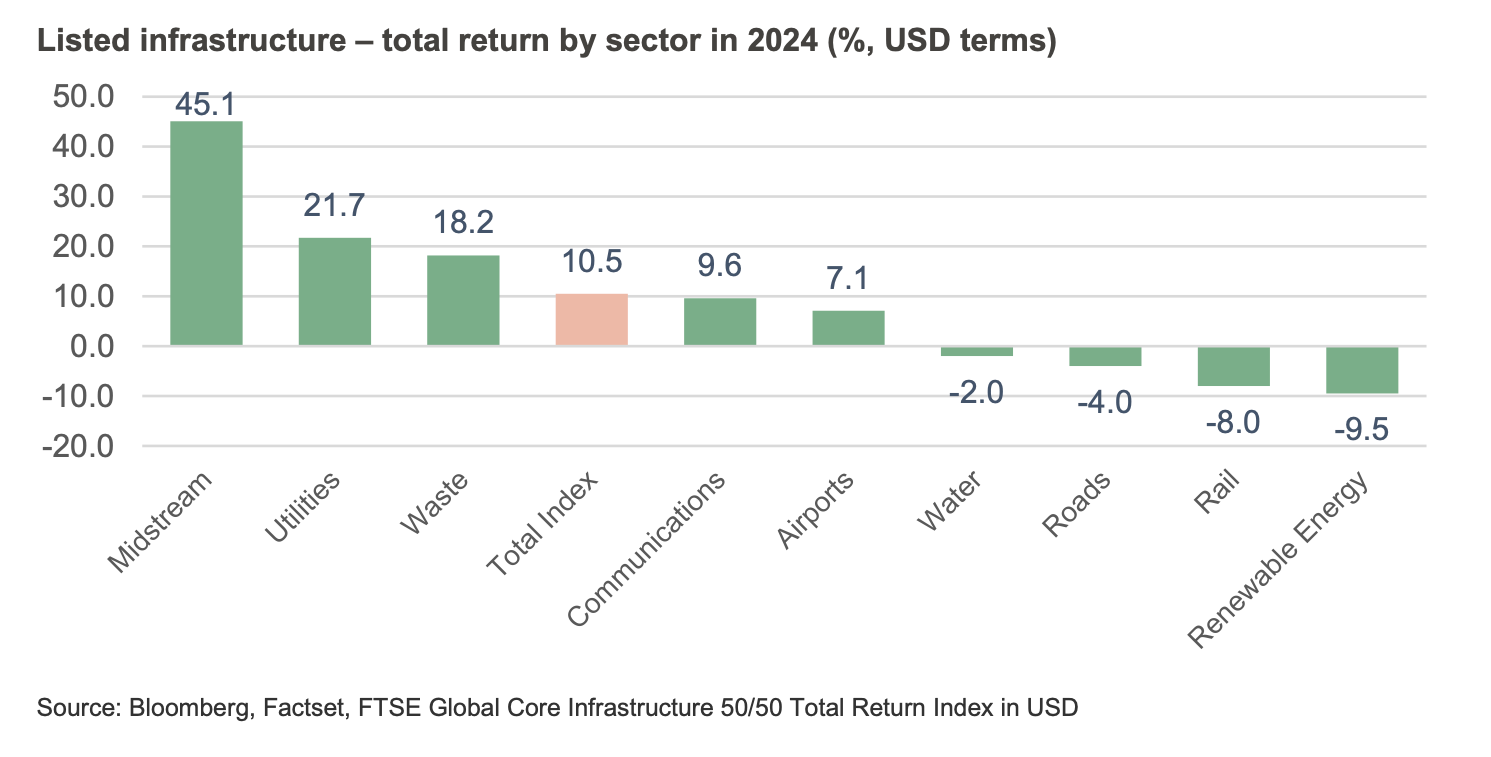

Listed infrastructure returned ~10%[1] in 2024. However, returns across subsectors varied widely as shown below.

AI was among the most powerful thematics for the year, creating a tailwind for several sectors:

- Midstream Infrastructure: Anticipated growth in fuel demand for electricity generation to power AI

- US Utilities: Increased electricity generation and transmission needs driving higher capital expenditure and earnings forecasts, and

- Communications Infrastructure: Rising demand for data centres, leading to higher leasing rates and new development opportunities.

Notably, the outperformance of Midstream and US Utilities also signalled an expected increase in carbon intensity to satisfy the demand for US power generation. Conversely, renewable energy faced challenges due to two factors: a Republican victory in the US elections that hurt the outlook for renewable development in the US, and stalled inflation progress in developed markets, leading to shifts in interest rate expectations.

ANTICIPATING 2025

While many long-term thematics such as digitalisation, climate change, aging populations and strained public finances remain as relevant as ever, many of the major near-term themes of 2024 remain highly relevant for 2025. Three of the most important considerations are:

- The return of the Trump administration and its policies (Trump 2.0)

- The continued growth of AI and the infrastructure required to support it

- Challenges to the energy transition

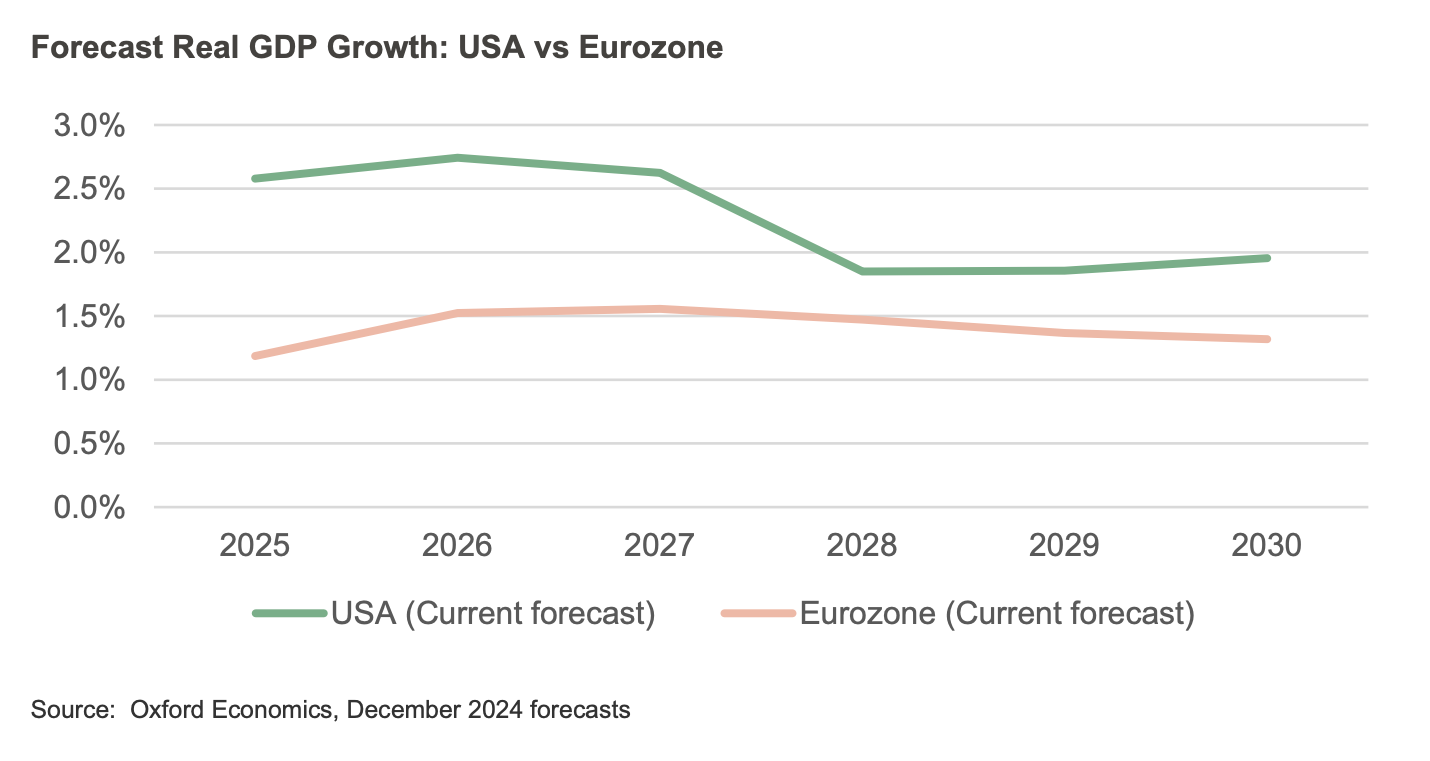

These themes will play out against a complex macroeconomic backdrop, where the US economy continues to demonstrate remarkable resilience while Europe and other regions grapple with recession risks. Infrastructure investments, which are noted for their defensiveness and growth potential, are poised to stand out, while listed infrastructure specifically enjoys additional benefits through its liquidity compared to unlisted alternatives.

ECONOMIC IMPLICATIONS OF TRUMP 2.0

The return of Donald Trump, supported by Republican control of Congress, sets the stage for transformative US policy shifts with few limitations. The implications of this political set-up are powerful and wide-ranging, and if Trump’s first term is any indication, unpredictability is to be expected in his second term. Early indications suggest a focus on protectionism, corporate tax cuts, expanded hydrocarbon production, and reduced support for renewable energy. These policies, many of which are inflationary, are expected to drive strong near-term economic growth in the US, strengthening the US Dollar and lifting US bond yields. Key sectors likely to benefit include GDP- sensitive infrastructure such as transportation (e.g., roads, railways), waste management, and energy transportation.

Conversely, Europe’s economic outlook remains fragile, as the region faces several key

challenges that the US does not, including:

- Higher energy costs – Europe’s reliance on imported natural gas and oil leaves it open to fluctuations in commodity markets

- Geopolitical uncertainties – ongoing conflict in eastern Europe, continuing to impact commodity prices, supply chains, and forcing higher government spending on defence

- Lack of innovation – Europe continues to struggle to develop technology companies, with the continent still without a home-grown ‘hyperscaler’ technology company

- Tighter regulations – Europe’s regulatory environment is generally more rigid than the US, which acts as a headwind to business formation and business scaling

- Challenging demographics – many European countries face aging populations and declining birth rates, shrinking the workforce and lowering potential growth

- Potential US tariffs may represent an additional and meaningful headwind for Europe

Despite these challenges, opportunities in the European market remain. Governments are focused on driving economic growth, and there is a pressing need for investment in energy infrastructure. Many European utilities have ambitious capital expenditure programs aimed at delivering grid resilience, alongside the important development of renewable energy generation assets. For example, business plans submitted in 2024 by UK electricity transmission utilities

included over £67b of total expenditure over six years – a 6x increase from the 2019 regulatory cycle. Investments of this nature represent the backbone of the energy transition, and investments of this scale represent major growth drivers for the broader economy.

Investment into European renewable energy and associated infrastructure remains essential to ensure energy security and independence, regardless of headwinds to the energy transition elsewhere. While Europe’s energy import dependence has declined since the conflict in eastern Europe commenced in 2022, Europe’s reliance on both Russian and US LNG persists, underscoring the need for continued energy investment to meet energy security objectives.

The divergent outlook for economic growth in Europe compared to the US drives an unusual dynamic when analysing investment opportunities, creating a more favourable outlook for rate-sensitive sectors in Europe. Utilities, renewable energy and communications infrastructure are of particular interest.

ARTIFICIAL INTELLIGENCE AS A TRANSFORMATIONAL FORCE

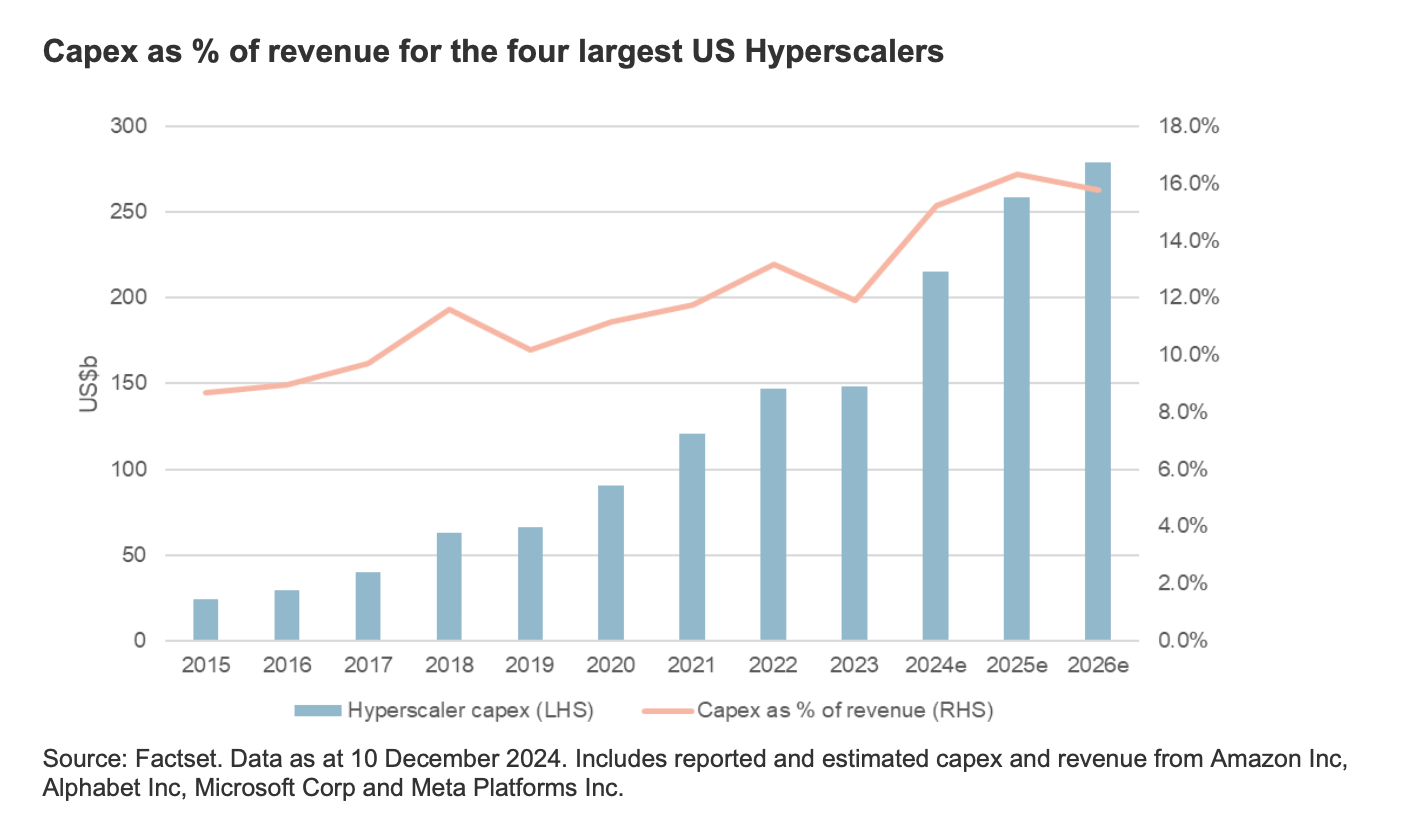

Since the release of ChatGPT in late 2022, AI and the hardware and infrastructure required to power it has captured the excitement of investors worldwide. In 2024, AI-driven development spurred demand for hardware, power, and communication infrastructure, with the International Energy Agency (IEA) forecasting that global data centre electricity usage may double by 2026, underscoring the amount of power demand growth.

The lifecycle of AI applications can generally be broken into the training and inferencing phases.Due to the highly intensive computational requirements of AI training, it is generally reliant on hyperscaler data centres and hardware (such as semiconductors), and hyperscalers have deployed significant resources internally for AI training. Increased capital expenditure from major hyperscalers in 2024 is likely to be eclipsed by even larger investments expected in 2025 and 2026.

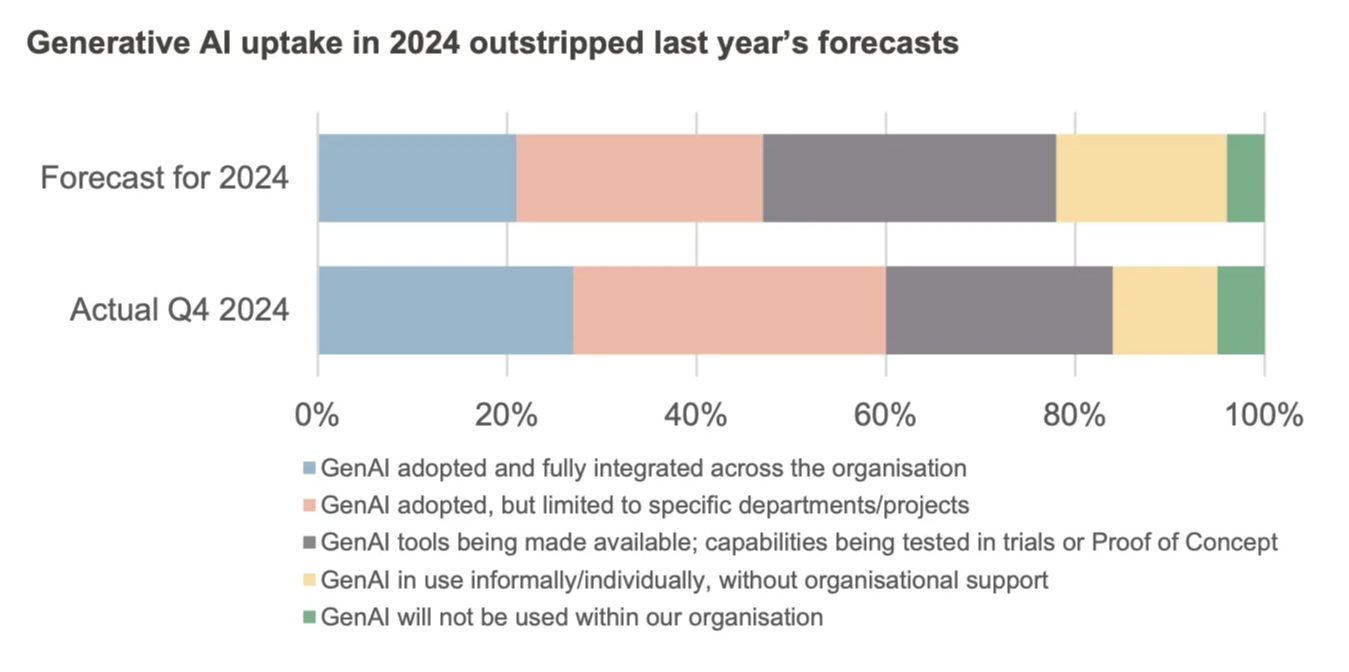

While 2024 saw significant investments into AI training capacity, substantial advancements in AI training and the development of new generations of AI hardware, 2025 is expected to see a meaningful uplift in demand for AI inferencing as AI software becomes more widely used. This comes as the uptake of Generative AI (focused on the creation of original content such as text and images) by businesses exceeded expectations in 2024.

AI applications, such as Microsoft Copilot, which rely heavily on inferencing to process inputs and generate intelligent, context-aware outputs, are set to expand in 2025, enhancing business productivity and user experience. This growth underscores the attractive outlook for sectors supporting AI inferencing, including communication networks, edge data centres, and energy transportation infrastructure.

Importantly, monetisation is expected to become more visible at the inferencing stage. Attractive financial returns from AI applications is likely to spur further investments by hyperscalers, benefitting the infrastructure required to train and deliver AI. Sectors such as US utilities, independent power producers and data centres, performed very strongly in 2024 driven by AI training demand, with growth likely to remain relatively high if current and emerging applications gain widespread adoption and generate strong financial returns.

Despite AI’s promising outlook, challenges persist, particularly in the data centre sector, where surging demand for AI infrastructure has driven a major increase in data centre building activity. This has led to meaningful labour shortages for key roles in many data centres markets in the US. While higher salaries can help, the limited skilled workforce restricts development speed, making labour supply a key risk in AI deployment and related infrastructure demand.

Finally, the geographic outlook for AI favours the US, home to several major hyperscalers and the world’s largest data centre market and a net exporter of energy. Conversely, Europe faces disadvantages in these critical areas, making the US considerably more attractive than Europe for AI infrastructure growth.

ENERGY TRANSITION CHALLENGES

Morrison’s investment philosophy is to invest wisely in ideas that matter. We believe that Environmental, Social and Governance (ESG) factors have an impact on investment performance and valuation, and effective integration drives value across all time horizons.

Economic pressures and political shifts have recently created significant headwinds for sectors and companies that are well aligned with, and benefit from investor interest in, ESG considerations. In this regard, the energy transition is particularly topical.

By late 2024, the Republican sweep and Trump’s expected policies, including expanded drilling and withdrawal from the Paris Agreement, cast a shadow on US energy transition prospects. State-level anti-ESG measures, such as the 2021 ban in Texas on fossil fuel divestment and Florida’s 2022 restrictions on ESG considerations in state fund management, add further pressure.

Some major asset managers have adapted to shifting dynamics. Over the past year, BlackRock, once a strong ESG advocate, exited the Net Zero Asset Managers initiative, cut support for ESG proposals from 47% in 2021 to 4%, and allowed institutional clients to vote against such proposals. With the US firmly under Republican leadership until at least 2026, the outlook remains challenging for energy transition-focused sectors.

Despite these challenges, regions like Europe and China remain strongly committed to renewable energy and their ambitions stand out in stark contrast to the expected direction of US policy. This underscores the importance of regional selectivity when targeting ESG-driven opportunities.

2024 was the warmest year on record, and 2025 commenced with catastrophic wildfires in Southern California, likely linked to climate change. This tragedy unfolds as the new US administration, many of whom are sceptical of climate change, takes office. This underscores the difficult backdrop for energy transition investments in the US.

Reduced near-term carbon reduction efforts will likely necessitate accelerated efforts in the medium-term. Accordingly, this creates a nuanced outlook for ESG-positive sectors such as renewable energy; challenging in the near-term, but highly attractive in the medium to long-term. This is likely to create attractively priced opportunities for long-term investors.

CONCLUSION

In 2025, powerful political and societal shifts, technological advancements and macroeconomic divergence are expected to be among the key drivers of investment performance. Listed infrastructure stands out as a compelling asset class, offering an attractive blend of defensiveness, growth and liquidity. However, regional disparities and evolving policy environments demand a selective and thematic approach.

Morrison remains committed to uncovering the best risk-adjusted returns by harnessing long-term thematics while adapting to near-term dynamics. Our key views are that:

- Trump’s second term will drive strong economic performance in the US, particularly benefitting GDP-linked infrastructure

- AI inferencing will become more widespread, benefitting infrastructure closer to users, such as communications networks. This will be particularly evident in the US

- The energy transition will slow in certain regions, but the long-term direction remains clear, offering opportunities for investors looking beyond the short-term

As the year unfolds, opportunities will emerge for investors who balance discipline with foresight.

DISCLAIMER

MARKETING COMMUNICATION

This communication is directed at professional clients.

The statements and opinions expressed in this document and any related discussions (the Document) are based on the information available as at the date of the Document (January 2025) and the information is preliminary in nature only and subject to change, which may be material, at any time without notice. Morrison Private Markets Pty Limited (ABN 71 136 338 906, AFSL No 340502) including its related companies and their respective directors, employees, advisors and shareholders (“Morrison”) reserves the right, but will be under no obligation, to review or amend the Document.

In the UK this Document is issued by Morrison Infrastructure (UK) Limited, Registered in England & Wales under number 11292181. Registered office: CityPoint, 1 Ropemaker St, London EC2Y 9SS. Authorised and regulated by the Financial Conduct Authority.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU). This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The Document and all other information made available to the recipient in connection with it (additional information) do not constitute an offer to invest or the solicitation of an offer to invest or an offer to provide investment management services in any jurisdiction and no such solicitation will be made or offer accepted in the future unless in accordance with appropriate regulatory authorisations in all relevant jurisdictions. The document is not personal financial advice and is not a recommendation by Morrison to make an investment. This Document has been prepared without taking into account the investment objectives, financial situation or particular needs of any particular person or entity. Before making an investment decision, you should consider, with or without the assistance of a financial adviser, whether any investments are appropriate in light of your particular investment needs, objectives and financial circumstances. Nothing contained herein should be construed as legal, business or tax advice and each prospective investor should consult its own advisers as to legal business, financial, tax and related matters concerning the information contained in the Document.

Any person who is in possession of this document is hereby notified that no action has or will be taken that would allow a direct or indirect offering or placement of the units to retail investors in any jurisdiction. No person guarantees the performance of, or rate of return from, products listed in this Document, nor the repayment of capital in relation to an investment in it.

In preparing the Document, Morrison has relied on forecasts and assumptions about future events which, by their nature, are not able to be verified. Inevitably some assumptions may not materialise and unanticipated events and circumstances are likely to occur. Therefore, actual results in the future will vary from the forecasts which Morrison has relied for the purposes of the Document. These variations may be material. Past performance is not a guide to future performance

References to specific company stocks should not be construed as recommendations or investment advice. The statements and opinions are subject to change at any time, based on market and other conditions. Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions. Investing involves risk including the risk of loss of principal.

In addition, the Document contains information sourced from third parties which has not been independently verified. Morrison will not be liable to any recipient for errors or omissions from the Document, whether arising out of negligence or otherwise.

[1] Represented by the FTSE Global Core Infrastructure 50/50 Total Return Index in USD